Every year, millions of homeowners face devastating financial losses from floods, and yet, only a given percentage of U.S. households have flood insurance. With natural disasters causing billions in insured losses globally each year, the risk has never been higher.

Understanding flood insurance statistics is crucial for homeowners, businesses, and policymakers to assess exposure, make informed decisions, and protect what matters most. Our team at Healthsure Hub dives deep into the latest numbers, trends, and insights shaping the flood insurance industry, offering actionable takeaways to stay ahead of the risks.

Top Flood Insurance Statistics

The following flood insurance statistics highlight the current state of coverage, market growth, and protection gaps in the U.S. and globally:

- 4.7 million active flood insurance policies are held through the U.S. National Flood Insurance Program (NFIP).

- Only 3.3% of U.S. households have flood insurance coverage.

- 569,000 private residential flood insurance policies exist in the U.S., nearly doubling since 2020.

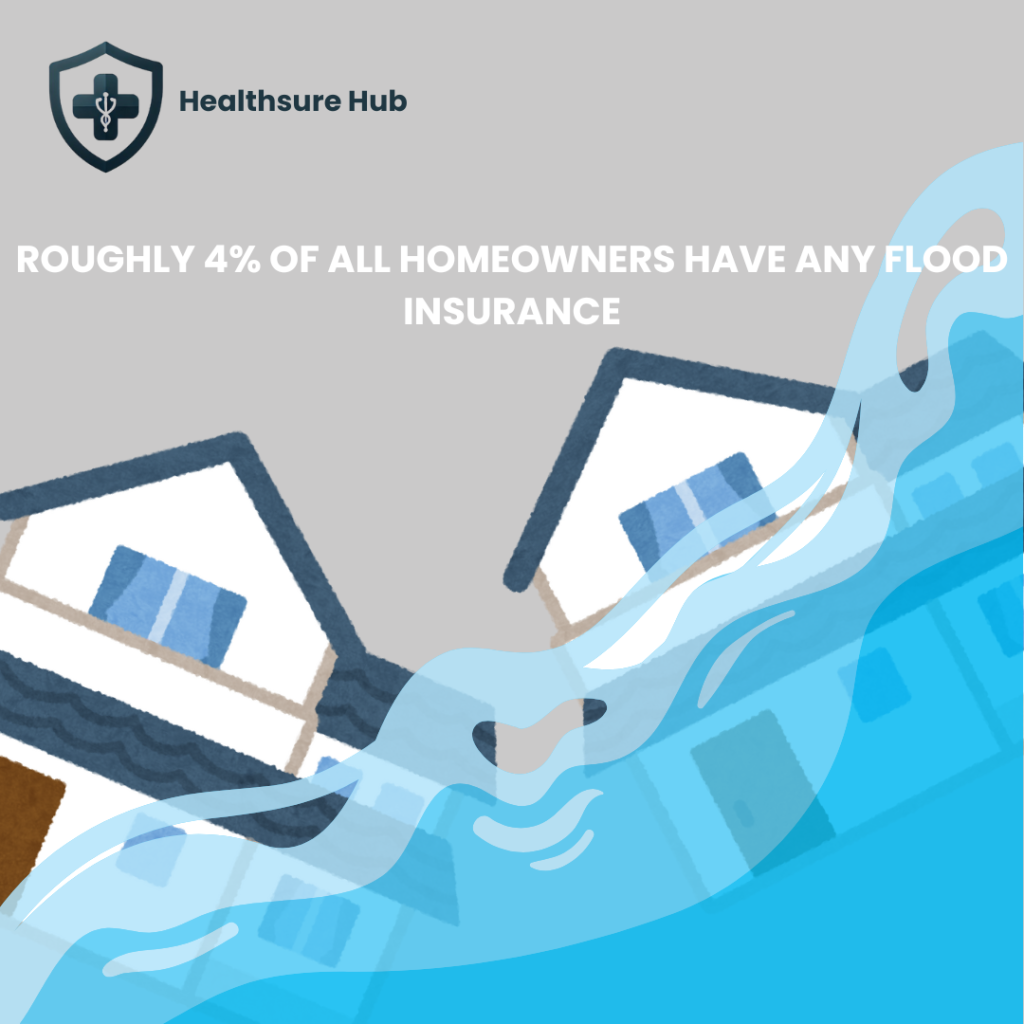

- Only 4% of U.S. homeowners have flood insurance

- The average NFIP premium in 2025 is approximately $899 per year.

- NFIP total coverage in force exceeds $1.3 trillion.

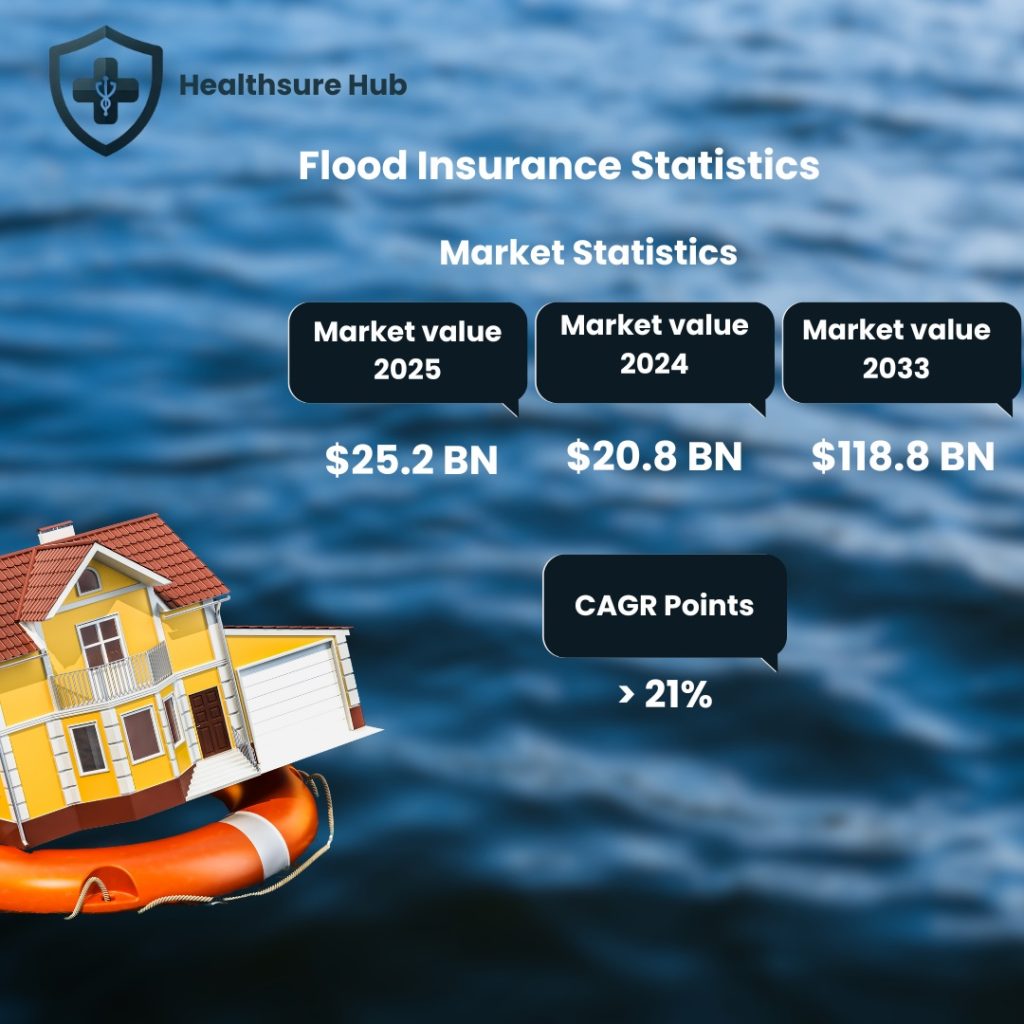

- The global flood insurance market is valued at around $25.2 billion in 2025, up from $20.8 billion in 2024.

- Forecasts predict the global market could reach $118.8 billion by 2033, with a CAGR of 21%.

- Private flood insurance loss ratios in the U.S. are generally below 50%, indicating profitability.

- Adoption of flood insurance is growing due to climate change, increased flood frequency, and regulatory pressure.

- Technological innovations such as AI-driven risk modeling, GIS mapping, and parametric insurance are transforming flood insurance pricing and claims management.

- Natural catastrophe insured losses globally exceed $100 billion annually; severe weather events (storms, floods) are intensifying demand for coverage.

Taken together, these flood insurance statistics reveal strong growth potential alongside significant protection gaps that still leave millions financially exposed.

Global Flood Insurance Market Trends

Global flood insurance statistics show rapid market expansion. Valued at $25.2 billion in 2025, up from $20.8 billion in 2024, the market is projected to reach $118.8 billion by 2033, representing a CAGR of 21%. Growth is fueled by several factors:

- Increasing frequency of floods and natural disasters. Rising sea levels, extreme rainfall, and storm surges are driving both demand and risk awareness.

- Expansion of private flood insurance markets. Private insurers complement public programs, offering more flexibility and coverage options.

- Regulatory pressures. Governments are increasingly mandating insurance in high-risk zones to reduce disaster-related losses.

- Technological innovations. AI, GIS, and parametric insurance improve risk assessment, pricing, and claims efficiency.

A Deep Dive into the U.S. Flood Insurance Statistics

When examining flood insurance statistics in the United States, the market is largely shaped by the National Flood Insurance Program, alongside a fast-growing private sector. Together, they form the backbone of flood risk protection for American homeowners.

NFIP Policies and Coverage

The National Flood Insurance Program (NFIP) currently supports about 4.7 million active policies, with total coverage exceeding $1.3 trillion. These policies help homeowners in flood-prone areas, especially where private insurance is not available or is too expensive.

NFIP policies offer standardized protection, covering both the structure of the home and personal property. In many cases, lenders require NFIP coverage for homes located in high-risk flood zones.

Private Flood Insurance

The private flood insurance market is expanding, with roughly 569,000 residential policies in place as of 2024, almost double the number from 2020. Private insurers offer benefits such as higher coverage limits, faster claims processing, and more flexible policy terms.

Private flood insurance is also profitable for insurers, with loss ratios typically below 50%, encouraging more companies to enter the market and serve homeowners who might otherwise be uninsured. Private insurance often offers:

- Higher coverage limits than NFIP

- Faster claims processing

- Flexible policy terms

Coverage Gaps

Despite growth, flood insurance statistics clearly show a persistent protection gap. Only 3.3% of U.S. households are covered by NFIP policies, and roughly 4% of all homeowners have any flood insurance at all. This underlines the vulnerability of millions of Americans, particularly in inland and lower-risk areas that are increasingly exposed to flooding due to climate change.

Rising Natural Catastrophe Losses Are Driving Flood Insurance Demand

Natural disasters are becoming more costly every year. Global insured losses from natural catastrophes now exceed $100 billion annually, with floods and severe storms accounting for a growing share of those losses.

This surge in damage is not limited to coastal regions. Inland flooding, flash floods, and extreme rainfall events are increasingly impacting areas that were once considered low risk. As a result, homeowners, insurers, and governments are reassessing how flood risk is measured and managed.

These escalating losses are a key reason why demand for flood insurance is intensifying worldwide. As extreme weather events become more frequent and severe, both public programs and private insurers are under pressure to expand coverage, improve risk modeling, and close long-standing protection gaps.

Drivers of Flood Insurance Adoption

Several factors are driving growth:

- Climate Change: More frequent and severe storms increase exposure.

- Regulatory Pressure: Mortgages in high-risk zones often mandate flood insurance.

- Urbanization: Expanding urban areas increase the number of properties at risk.

- Technological Innovation: GIS mapping, AI-driven risk modeling, and parametric insurance enhance pricing and claims efficiency.

For example, AI-driven modeling can predict flood risk for individual properties with high accuracy, allowing insurers to offer personalized premiums and expanding access to coverage in areas previously considered too risky.

Challenges in the Flood Insurance Market

While flood insurance statistics show growth, challenges remain. With only 4% of U.S. homeowners insured, most households remain financially exposed to flood damage.

Affordability is another major issue. Premiums can be costly in high-risk zones, and rising flood severity continues to pressure pricing. At the same time, the NFIP relies heavily on federal support, raising sustainability concerns after large-scale disasters.

Climate uncertainty further complicates underwriting and long-term planning for both public and private insurers.

Conclusion

Flood insurance remains a vital tool for mitigating financial risk. The latest flood insurance statistics show that only about 4% of U.S. homeowners are protected, while global market growth highlights enormous opportunities. As climate change and extreme weather events increase, the need for comprehensive flood coverage has never been greater. Homeowners, insurers, and policymakers must act now to close the protection gap, expand coverage, and leverage technology to make flood insurance more accessible and efficient.

Sources:

- https://www.globalgrowthinsights.com/market-reports/flood-insurance-market-110943

- https://www.congress.gov/crs-product/R44593

- https://coinlaw.io/flood-insurance-industry-statistics

- https://beinsure.com/news/us-private-flood-insurance-market-grown

- https://www.npr.org/2025/07/14/nx-s1-5464916/flood-insurance-extreme-weather-climate-change

- https://www.reuters.com/business/environment/global-insured-catastrophe-losses-set-hit-107-billion-2025-report-shows-2025-12-16