Choosing the right type of home insurance often feels simple, until you realize that not every home is insured the same way. The comparison between dwelling fire vs homeowners insurance is one of the most misunderstood topics in property insurance, yet it directly affects claim approvals, coverage gaps, and long-term financial protection. While both policies protect residential structures, they serve different purposes, apply to different living situations, and respond very differently when a loss occurs.

Understanding the real difference between dwelling fire vs homeowners insurance helps property owners avoid costly mistakes, especially as insurance carriers tighten underwriting standards and climate-related risks continue to rise.

Why Dwelling Fire vs Homeowners Insurance Is Often Confused

The confusion around dwelling fire vs homeowners insurance usually starts with language. A house is a dwelling, so it only seems logical to assume that all homes qualify for homeowners insurance. In practice, insurance companies care far more about how a property is used than what it is called. Occupancy status, length of vacancy, rental activity, and even geographic fire exposure all influence which policy applies.

Homeowners insurance is built for stability and daily occupancy, while dwelling fire insurance exists for flexibility and risk isolation. When the wrong policy is applied to the wrong situation, claims are often delayed, reduced, or denied entirely.

How Homeowners Insurance Works in Practice

Homeowners insurance is designed for owner-occupied primary residences, meaning the home where the policyholder lives most of the year. This policy assumes daily use, regular maintenance, and personal responsibility for what happens inside the property. Because of that assumption, homeowners insurance bundles several protections into a single policy. In fact, between 96% and 97% of all homeowners insurance claims involve damage to the home or personal property, highlighting the importance of adequate dwelling and belongings coverage.

In a dwelling fire vs homeowners insurance comparison, homeowners insurance stands out because it protects not only the structure but your belongings, as well. Coverage typically includes the dwelling itself, personal belongings, personal liability, and additional living expenses if the home becomes temporarily uninhabitable due to a covered loss. Mortgage lenders frequently require homeowners insurance because it reduces both borrower and lender risk.

What Dwelling Fire Insurance Is Designed to Do

Dwelling fire insurance protects the physical structure of non-owner-occupied homes, usually rentals, vacation homes or vacant houses. In most cases dwelling fire insurance insures residential structures that do not qualify for standard homeowners insurance. These properties may still be valuable, well-maintained, and fully occupied at times, but their usage patterns introduce risks that homeowners insurance is not designed to absorb.

Unlike homeowners insurance, dwelling fire insurance mainly covers the structure itself and specific perils with fire being the most central. Depending on the policy form, coverage may also extend to hazards like lightning, wind, vandalism, or water damage from sudden events.

Dwelling fire insurance is commonly used for rental properties, vacation homes, seasonal residences, vacant homes, Many dwelling fire policies are written for homes in regions prone to disasters, and statistics on property and casualty losses from catastrophes show how frequent and costly these events can be, helping homeowners and investors understand the potential risks.

While it can include optional protections such as loss of rental income, it does not automatically include liability coverage or personal property protection in the same way homeowners insurance does.

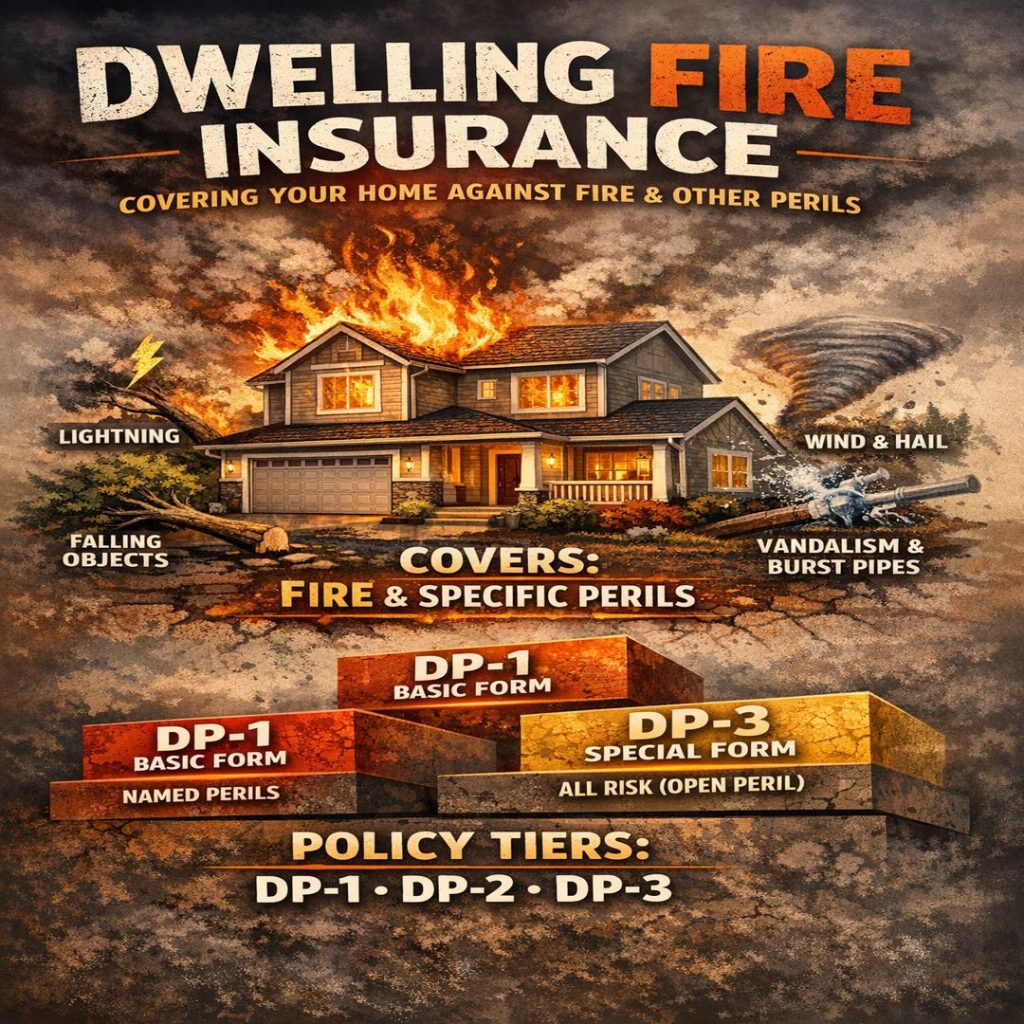

Policy Forms and Coverage Depth in Dwelling Fire Insurance

Dwelling fire insurance policies are commonly issued in tiers, often referred to as:

DP-1

The DP-1 policy is a basic coverage form, otherwise known as “named perils”. This policy type typically covers losses due to:

- Fire

- Lightning

- Internal explosion

Claims usually pay actual cash value, meaning replacement cost minus depreciation. This form works best for low-risk rental properties or simple coverage needs. Other perils, such as theft, vandalism, or floods, usually require extra endorsements.

DP-2

Also known as “named perils” policy, this insurance form covers the same perils as DP-1 with additional charges, but not limited to:

- Vandalism and malicious mischief

- Windstorm or hail

- Riot or civil commotion

- Vehicles

- Smoke

- Burglary damage

- Weight of ice and snow

- Sudden water damage

- Freezing

Insurance claims often pay full replacement cost for the building. It’s ideal for rental or second homes with moderate risk, though personal property and liability coverage must be added separately.

DP-3

The DP-3 form is the most exclusive coverage available. While the other two forms are known as “named perils”, DP-3 is referred to as “open perils” or “all risk” policy. This policy covers nearly all perils except those specifically excluded. Mostly it covers:

- Neglect

- Intentional loss

- Mold, rust, rot

- Constant or repeated leakage

Claims pay full replacement cost, making it a strong choice for landlords or investors seeking near-homeowners-level protection. Personal property, liability, and loss-of-income coverage still need to be added separately.

Each form reflects a different approach to risk and reimbursement. Basic forms cover a limited number of named perils and typically settle claims based on actual cash value. Broader forms expand the list of covered risks and often provide replacement cost coverage. The most comprehensive forms protect the dwelling against all perils except those specifically excluded, offering a level of protection closer to homeowners insurance but without personal coverage.

This tiered approach makes dwelling fire insurance flexible and especially useful for landlords and property investors.

Dwelling Fire vs Homeowners Insurance Occupancy

Occupancy is one of the most important differentiators when evaluating dwelling fire vs homeowners insurance. Insurance carriers assess risk based on who lives in the property, how often it is occupied, and who controls day-to-day activity.

A primary residence with consistent occupancy typically qualifies for homeowners insurance because risks are predictable and quickly detected. In contrast, rental properties and secondary homes often experience delayed discovery of damage, tenant-caused losses, or longer periods of vacancy, which increases the insurer’s exposure.

This is why dwelling fire insurance is frequently the correct choice even for well-maintained homes. It aligns coverage with real-world usage rather than forcing a policy that no longer matches the property’s function.

Coverage Scope in Dwelling Fire vs Homeowners Insurance

Homeowners insurance is comprehensive by design. It assumes the policyholder needs protection for the structure, personal belongings, legal liability, and temporary housing. This makes it ideal for full-time living situations but less adaptable when circumstances change.

Dwelling fire insurance, on the other hand, is modular. Coverage focuses on the structure and expands only when additional protections are selected. This approach allows property owners to insure buildings that fall outside standard guidelines while still controlling premium costs.

Because of this difference, dwelling fire insurance is often more affordable, but affordability should never be mistaken for adequacy. The true value of dwelling fire vs homeowners insurance depends on matching coverage scope to actual risk exposure.

Liability Exposure in Dwelling Fire vs Homeowners Insurance

Homeowners insurance automatically includes personal liability coverage, protecting the policyholder if someone is injured on the property or if accidental damage affects others. This coverage extends beyond the home and follows the insured in many everyday situations.

Dwelling fire insurance does not automatically provide the same level of liability protection. For rental properties, liability is often handled through endorsements or separate landlord liability policies. Without proper coverage, owners could be personally responsible for accidents or injuries on their property.

Cost Considerations

Dwelling fire insurance is generally less expensive because it insures fewer risks and excludes personal belongings and lifestyle-related claims.

However, underinsuring a property to save on premiums can create far greater losses later. Rising construction costs, supply chain disruptions, and labor shortages have significantly increased rebuild expenses in recent years. According to industry data, residential rebuilding costs have increased by more than 30 percent in many U.S. regions since 2020, making accurate dwelling limits more important than ever.

Choosing between dwelling fire vs homeowners insurance should always involve evaluating replacement cost accuracy, deductible structure, and risk exposure rather than focusing solely on monthly premiums.

Common Mistakes Property Owners Make

Many property owners unknowingly misapply homeowners insurance to rental or vacant properties, assuming coverage will remain valid. Others rely on dwelling fire insurance without addressing liability exposure or loss-of-income needs. These mistakes often surface only after a claim occurs, when options are limited.

The most effective way to avoid these issues is to reassess coverage whenever a property’s use changes. Even temporary changes, such as extended vacancy or short-term rental activity, can alter which policy is appropriate.

Conclusion

Understanding dwelling fire vs homeowners insurance empowers property owners to protect their investments with clarity and confidence. Both policies serve essential roles, but they are not interchangeable. As property usage evolves and insurance markets become more selective, choosing the right policy becomes less about labels and more about alignment.

When coverage accurately reflects how a property is used, insurance becomes what it is meant to be: a reliable safeguard, not an unexpected obstacle.