Dental care plays a critical role in overall health, yet access to dental insurance in the United States remains uneven and limited compared to medical coverage. While many Americans assume dental benefits function similarly to health insurance, the data tells a different story. Analyzing current dental insurance statistics reveals persistent coverage gaps, demographic disparities, and structural limitations that affect tens of millions of adults nationwide.

Healthsure Hub brings together the most reliable national data to explain how many adults lack dental insurance, who is most affected, why coverage lags behind medical insurance, and what these trends mean for public health and policy.

How Many Adults in the U.S. Lack Dental Insurance?

Recent nationally representative data shows that approximately 27% of U.S. adults—about 72 million people—do not have dental insurance. This figure is striking not only because of its size, but because it is nearly three times higher than the percentage of adults who lack health insurance.

Despite increased awareness of the link between oral health and systemic health, dental insurance coverage has not kept pace with medical insurance expansion. Understanding why requires looking deeper into how coverage varies by insurance type, age, income, and employment.

Dental Insurance Statistics by Coverage Type

Medicare beneficiaries

Roughly 31% of people enrolled in Medicare do not have dental insurance. This gap exists largely because traditional Medicare does not include routine dental services such as cleanings, fillings, crowns, or dentures. While some Medicare Advantage plans offer limited dental benefits, coverage varies widely and is often capped annually.

As a result, many older adults face high out-of-pocket costs precisely when dental needs increase due to age-related conditions such as gum disease, tooth loss, and dry mouth linked to medications.

Medicaid recipients

Among adults covered by Medicaid, dental insurance statistics show that about 33% lack dental insurance. While Medicaid is required to cover dental services for children, adult dental coverage is optional and varies significantly by state. Some states offer comprehensive benefits, others limit coverage to emergency services, and some provide no adult dental benefits at all.

These inconsistencies contribute heavily to the disparities reflected in national dental insurance statistics, particularly among low-income populations.

Adults without health insurance

The overlap between medical and dental uninsurance is substantial. More than 83% of adults without health insurance also lack dental insurance, compounding barriers to care. For these individuals, routine dental visits are often delayed until pain or infection requires emergency treatment.

Dental Insurance Coverage by Age Group

Age is a strong predictor of dental insurance coverage in the United States.

Young Adults

Young adults experience some of the highest uninsured rates for dental coverage. Many individuals in this age group lose coverage when they age out of their parents’ dental plans, often around age 26, and do not immediately replace it with employer-sponsored insurance.

Early-career employment is also more likely to involve part-time, temporary, or gig-based work, which frequently does not include dental benefits. Even when individual plans are available, younger adults may deprioritize dental insurance in favor of rent, student loan payments, or other essential expenses. This combination of transitional life stages and financial pressure contributes to lower enrollment rates, despite the long-term benefits of preventive dental care.

Middle-Aged Adults

Adults between the ages of 30 and 59 are the most likely to have dental insurance coverage. This group benefits from higher rates of full-time employment and greater access to employer-sponsored dental plans, which remain the primary source of coverage in the U.S. Many individuals in this age range also have dependents, increasing the likelihood of enrolling in family dental plans as part of a broader benefits package.

As a result, this group anchors overall coverage rates and can mask disparities seen in younger and older populations when reviewing aggregated dental insurance statistics. However, coverage within this group is still vulnerable to job loss, career transitions, or shifts toward self-employment, which can quickly disrupt access to dental benefits.

Older Adults

Dental insurance coverage declines again among adults aged 55 and older, particularly after retirement. Dental insurance statistics show that around 31 million individuals aged over 55 lack dental insurance putting them at a greater risk of many health and oral issues, whereas 39% of older adults have some kind of dental coverage from public programs.

Many individuals lose access to employer-sponsored dental plans when they exit the workforce and transition to Medicare, which does not include routine dental benefits. While some seniors enroll in Medicare Advantage plans or purchase standalone dental policies, coverage is often limited by annual maximums, exclusions, and affordability concerns.

Dental Insurance Coverage by Income and Education

Socioeconomic status strongly influences access to dental insurance. 40% of adults earning under $30,000 per year and those without a high school diploma report significantly higher uninsured rates than higher-income and college-educated individuals.

These patterns highlight how affordability and plan design shape dental insurance statistics. Even when coverage is available, premiums, deductibles, and annual benefit caps can discourage enrollment among lower-income households.

Employer-Sponsored Dental Insurance Stats

Employer-sponsored plans remain the dominant source of dental insurance of the U.S. dental insurance market. Businesses consider dental insurance an appealing benefit in the employee benefits package. in the U.S. Most insured adults receive coverage through their jobs, often bundled with medical and vision benefits.

While this model expands access for working-age adults, it also creates instability. Job loss, retirement, or shifts to contract work frequently result in immediate loss of dental coverage. This dependence on employment is a key reason dental insurance statistics fluctuate more sharply across age groups than medical insurance data.

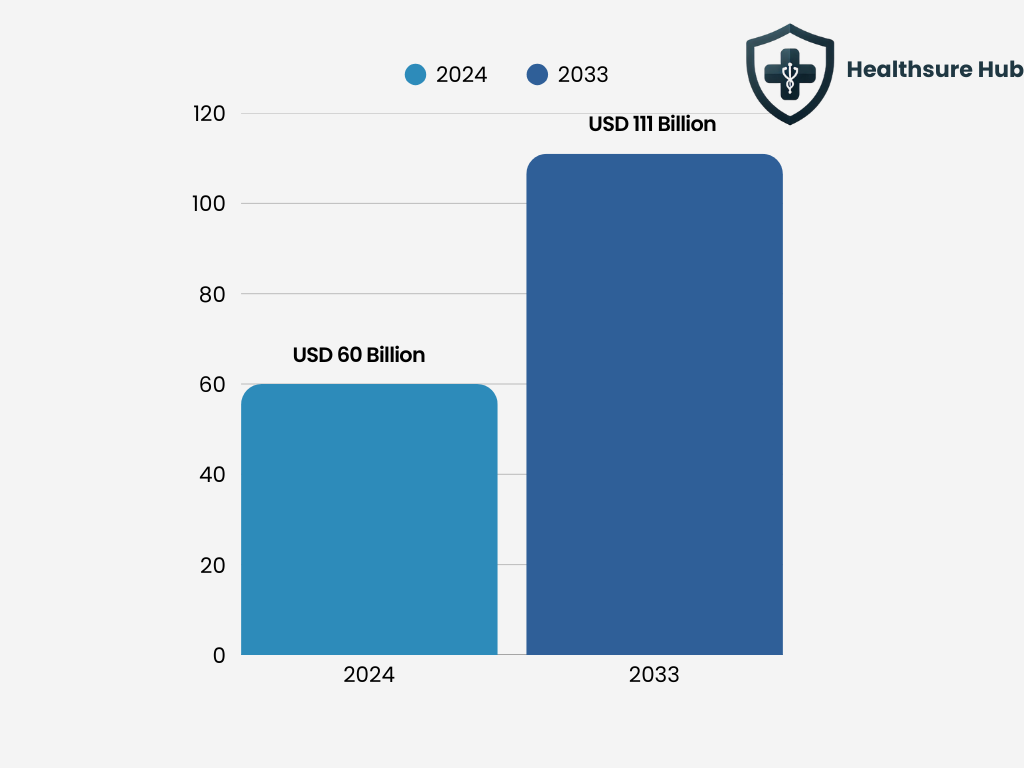

U.S. Dental Insurance Statistics and Market Growth

The U.S. dental insurance market has grown significantly in recent years. Industry forecasts estimate the market will expand from approximately $60 billion in 2024 to more than $110 billion by 2033, reflecting steady annual growth.

However, rising market value does not translate into universal coverage. These dental insurance statistics reveal a paradox: the industry is expanding financially while millions of adults remain uninsured or underinsured. Growth is driven largely by employer plans, population growth, and increased utilization among those already covered, not by closing coverage gaps.

Why Dental Insurance Lags Behind Medical Insurance

Dental insurance operates under a fundamentally different model than health insurance. Most plans emphasize preventive care and include:

- Annual maximum benefit limits

- Significant exclusions for major procedures

- Waiting periods for advanced services

As a result, dental insurance often functions more like a discount plan than true risk protection. These structural differences explain why dental insurance statistics consistently show higher uninsured and underinsured rates compared to medical insurance.

Health Consequences of Lacking Dental Insurance

The absence of dental coverage has measurable health consequences. Adults without dental insurance are more likely to delay care, resulting in advanced disease that is more expensive and difficult to treat.

Research consistently links poor oral health to systemic conditions such as diabetes, cardiovascular disease, respiratory infections, and cognitive decline. Dental insurance statistics therefore serve as indirect indicators of broader public health risks.

Emergency department visits for preventable dental conditions are also more common among uninsured adults, increasing healthcare costs without addressing underlying oral health needs.

Lack of dental insurance places adults at a significantly higher risk for delayed or avoided dental treatment, which often leads to the progression of preventable oral health conditions. When individuals do not have coverage, routine services such as cleanings, examinations, and early interventions are frequently postponed due to cost concerns.

Over time, minor issues like gingivitis or small cavities can progress into advanced periodontal disease, severe infections, tooth loss, and chronic pain. These outcomes are not only more difficult and expensive to treat, but they also have lasting effects on overall health and quality of life.

Conclusion

Current dental insurance statistics paint a clear picture: tens of millions of adults in the U.S. lack dental coverage, with disparities driven by age, income, employment, and policy design. While the dental insurance market is expanding, coverage gaps remain deeply entrenched.

Addressing these gaps will require more than market growth. It will require policy action, benefit reform, and recognition that oral health is inseparable from overall health. Until then, dental insurance statistics will continue to reflect unequal access to one of the most essential components of preventive care.

Sources:

https://carequest.org/new-report-72-million-adults-in-the-us-lack-dental-insurance-nearly-three-times-the-number-without-health-insurance-2/

https://carequest.org/out-of-pocket-a-snapshot-of-adults-dental-and-medical-care-coverage/

https://finance.yahoo.com/news/united-states-dental-insurance-market-102300046.html