Most people don’t buy life insurance because they’re thinking about death — they buy it because they’re thinking about life. Their children. Their spouse. Their mortgage. Their dreams of leaving something behind. Life insurance has always been one of the most personal financial decisions a family can make. It represents stability, dignity, and the reassurance that even if the unthinkable happens, the people you love won’t face the burden alone.

One thing remains clear as day— the life insurance industry is changing faster than ever. From rising premiums and coverage gaps to digital underwriting, shifting demographics, and new transparency rules, today’s landscape looks nothing like it did even five years ago.

To bring clarity, our team at HealthsureHub analyzed federal market reports, financial filings, insurer transparency disclosures, and consumer behavior studies to produce the most comprehensive, trustworthy, and up-to-date guide on life insurance industry statistics.

Key Life Insurance Industry Statistics

Before diving deeper, here are the top insights every consumer should know — insights that anchor today’s most important life insurance industry statistics:

- 51% of Americans currently own some sort of life insurance.

The life insurance coverage gap in 2021 exceeded $12 trillion, marking the largest shortfall ever recorded. - Millennials represent the fastest-growing market segment, but still have the lowest overall coverage rate.

- 55% of Americans in 2025 have life-insurance managed through their employer

- Digital underwriting adoption surged 65% since 2020, drastically reducing approval times.

- Men have higher life insurance rates compared to women.

- 92% of consumers purchased life insurance through online platforms

- More than 6 in 10 younger adults trust social media influencers in making the final purchase about insurance products.

- Life premiums climbed to €2.9 trillion in 2024.

- 42% of U.S. adults said they needed life insurance in 2024 and only 37% planned on actually buying.

Life Insurance Ownership

Life insurance ownership in the United States continues to grow, but only gradually. In 2025, 51% of Americans own some form of life insurance, showing steady—though modest—progress compared to previous years. From 2024, we can see just 1% of steady growth. Yet this growth hides a deeper issue: more than 49% of adults remain uninsured or underinsured, leaving millions financially vulnerable if a sudden loss occurs.

This gap between awareness and action is becoming more pronounced. In 2024, 42% of U.S. adults said they needed life insurance, but only 37% planned to purchase a policy. Even as more Americans acknowledge the importance of coverage, far fewer follow through.

This “intention gap” is now a core theme in modern life insurance industry statistics, signaling a growing disconnect between perceived need and real-world behavior.

The Growing Coverage Crisis

This intention gap contributes to a massive coverage shortfall across the country. The U.S. life insurance coverage gap surpassed $12 trillion in 2021, marking the largest deficit ever recorded. This crisis reflects a widening disconnect between the protection families need and the coverage their current policies actually provide.

It means the typical American household would face a substantial financial strain if a primary earner passed away—despite believing they are adequately protected.

Employer-Sponsored Coverage Dominates the Market

One of the main reasons for this mismatch is the heavy reliance on employer-sponsored plans. By 2025, 55% of Americans depend on life insurance provided through their employer. For a significant portion of these individuals, this workplace benefit is their only coverage.

While convenient, employer-based policies often fall short in two critical ways:

- Coverage amounts may be far lower than what families truly need

- Policies typically end when the individual leaves or changes jobs

These innovations make policies easier to obtain — especially for younger or first-time buyers — and represent some of the most influential life insurance industry statistics of the decade.

Global Life Insurance Premiums Continue to Climb

Despite coverage gaps in the U.S., international demand for life insurance remains strong. In 2024, global life premiums climbed to €2.9 trillion, fueled by rising financial literacy, expanding middle classes, and the rapid growth of digital distribution channels worldwide. This global momentum underscores a universal truth: more individuals and families are realizing the importance of long-term financial protection.

Digital Transformation Accelerates Underwriting and Access

Amid these structural challenges, the industry is transforming rapidly thanks to digital innovation. Since 2020, digital underwriting adoption has surged 65%, reshaping how Americans apply for and receive life insurance. What once took weeks can now be completed in days—or even minutes.

This shift is driven by:

- Automated risk assessment algorithms

- AI-assisted decision-making

- Electronic health records

- Simplified online applications

Together, these advancements are making life insurance more accessible, faster to obtain, and less intimidating for younger and tech-savvy consumers.

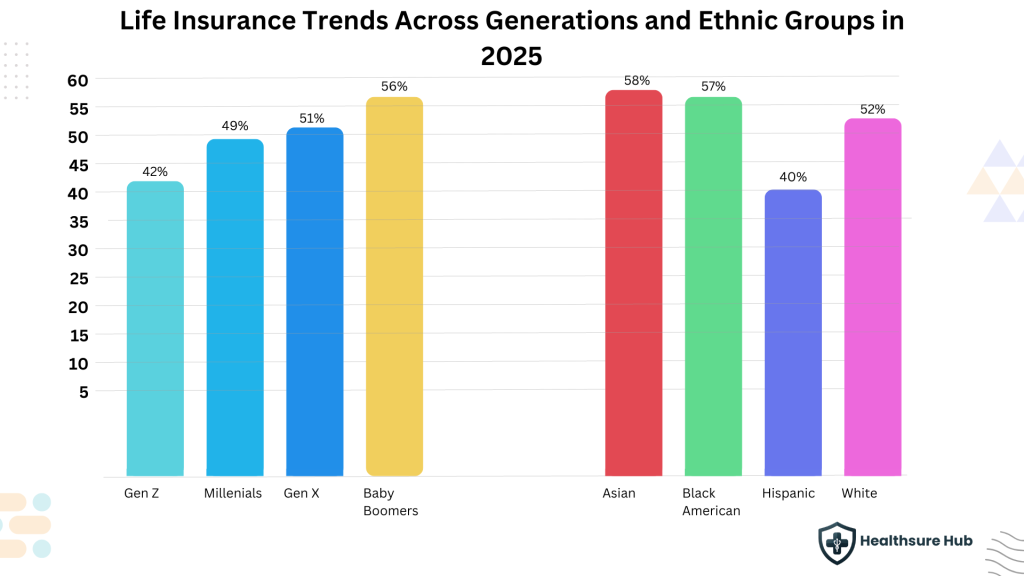

Life Insurance Trends Across Generations and Ethnic Groups in 2025

Younger adults continue to lag behind older generations, with Gen Z reporting just 42% coverage, the lowest among all age groups. Ownership increases steadily with age: Millennials reach 49%, Gen X climbs slightly higher at 51%, and Baby Boomers lead all generations at 56%. This reinforces a long-standing trend—older adults are far more likely to secure life insurance as financial responsibilities, health concerns, and estate planning become more urgent.

There are also notable differences across ethnic groups. Asian adults show the highest life insurance ownership rate at 58%, closely followed by Black Americans at 57%. White adults sit at 52%, slightly above the national average, while Hispanic adults have the lowest ownership rate at 40%. These disparities highlight varying levels of financial literacy, cultural attitudes toward financial planning, access to employer benefits, and perceived affordability across communities.

One noticeable thing in 2025 is that younger consumers are underinsured, and coverage rates remain uneven across racial and ethnic groups. For insurers, policymakers, and financial educators, these gaps point to a growing need for targeted outreach, simplified products, and better education to ensure more equitable access to life insurance protection.

The Persistent Gender Gap in Life Insurance Ownership

The gender divide in life insurance ownership continues to widen, even as awareness grows. In 2025, men were more likely than women to report owning life insurance—54% compared to 48%. While this difference may seem modest, it reflects a long-standing pattern that has shown little improvement over time.

The gap was even more pronounced just a year earlier. In 2024, only 46% of women owned life insurance, while 57% of men reported having coverage.

Many women recognize this shortfall: in 2024, 45%—representing 56 million individuals—said they had a coverage gap, and 37% planned to buy life insurance within the year. Yet ownership rates continue to lag.

Even among those who do have coverage, men still maintain an advantage through employer-sponsored plans. 46% of male policyholders say they have life insurance through their employer, compared to 43% of women.

Overall, the data shows a clear and ongoing trend: women remain significantly underinsured compared to men, despite increasing awareness and intent to close the gap.

The Digital Transformation of Life Insurance in 2025

The life insurance marketplace has undergone a dramatic digital shift over the last decade. In 2015, just 71% of Americans researched life insurance online—but by 2025, that number has surged to 92%, making the internet the primary starting point for nearly every consumer. Today’s buyers expect instant quotes, transparent comparisons, and easy-to-understand policy breakdowns, all of which have pushed insurers to improve their digital experiences. In fact, one in four Americans (25%) say they would not only research but also purchase life insurance entirely online, skipping in-person appointments altogether.

Yet surprisingly, Gen Z adults are the generation that would refer to other sources before making a life insurance purchase. Despite being the most digital-native generation, many Gen Z consumers show a stronger preference for hybrid shopping, seeking online information but still wanting a conversation with a real advisor before committing. This highlights a growing truth in the life insurance industry: while technology is reshaping how people shop, human guidance still matters, especially for younger adults navigating financial products for the first time.

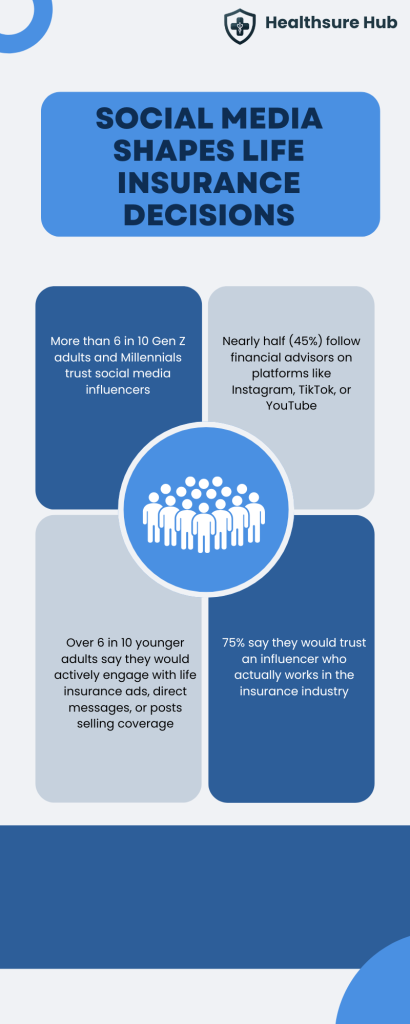

Social Media Shapes Life Insurance Decisions

Social media has become a powerful force in how younger adults learn about and shop for life insurance. More than 6 in 10 Gen Z adults and Millennials trust social media influencers to provide information about insurance products—a dramatic shift in how financial education is consumed.

Younger consumers are not just passively scrolling, either. Nearly half (45%) follow financial advisors on platforms like Instagram, TikTok, or YouTube, while over one-third follow insurance companies directly for updates, tips, and policy explanations. For these generations, social media has replaced the old model of brochures and in-office consultations, becoming a primary source of financial literacy.

Connection matters, too. More than half of younger adults say it is very or extremely important to stay in touch with their financial professional via social media channels. And their engagement goes beyond education—over 6 in 10 younger adults say they would actively engage with life insurance ads, direct messages, or posts selling coverage. This shows a growing openness to digital marketing and a willingness to explore and purchase life insurance right where they already spend their time: on social platforms.

Conclusion

The modern insurance landscape is no longer defined by static trends — it is driven by technology, shifting demographics, and rising financial awareness. The latest life insurance industry statistics reveal four powerful truths:

- Coverage gaps remain dangerously high, leaving millions exposed.

- Employer plans alone are not enough, especially during job changes.

- Digital tools are transforming how people shop, compare, and purchase coverage.

- Younger, diverse, and digitally connected consumers are redefining the future of protection.

For families, this means now is the time to reassess coverage, close gaps, and ensure financial security matches real-world needs. For insurers, it signals an urgent need for clearer products, faster digital processes, and more inclusive outreach.

As the numbers make clear, the path forward is simple: better education, smarter tools, and more accessible options — all guided by the evolving landscape of life insurance industry statistics.

Sources:

https://www.limra.com/siteassets/newsroom/liam/2025/2025_facts_about_life_insurance.pdf

https://www.limra.com/en/newsroom/news-releases/2024/u.s.-life-insurance-need-gap-grows-in-2024

https://beinsure.com/news/consumers-want-ai-to-simplify-life-insurance