Medical debt affects tens of millions of adults in the United States and represents one of the largest sources of household financial strain nationwide. Even in a system where the vast majority of Americans carry health insurance, unpaid medical bills continue to accumulate across income, age, and health status groups.

National survey data shows that medical debt statistics is not a fringe issue limited to the uninsured. Instead, it is a structural problem embedded in the way healthcare is financed, billed, and paid for in the U.S. Healthsure Hub’s data on medical debt show the true scope of the problem, the populations most at risk, and the broader consequences for households and healthcare providers.

How Common Is Medical Debt in the United States?

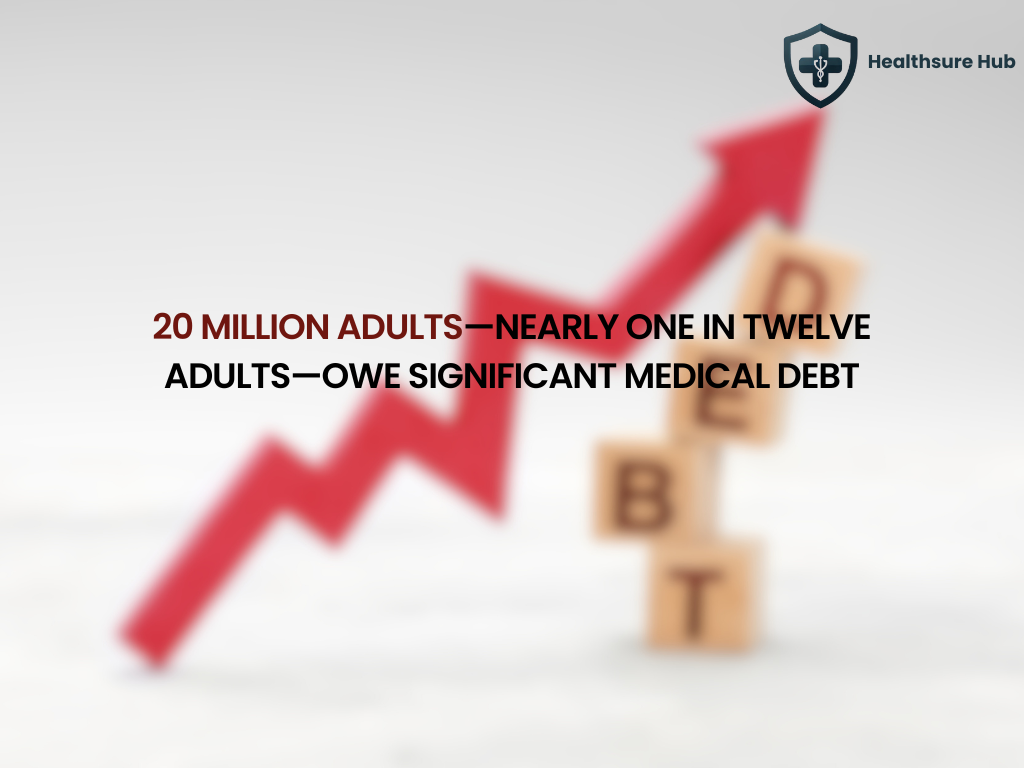

Medical debt remains widespread across the U.S. adult population. Survey data from the Census Bureau’s Survey of Income and Program Participation (SIPP) shows that approximately 20 million adults—nearly one in twelve adults—owe significant medical debt, or at least $220 billion in unpaid medical bills.

At the household level, medical debt is similarly prevalent. The analysis indicates that 15% of U.S. households carried medical debt in 2021, while broader polling definitions that include credit cards and informal borrowing suggest the true share of households affected is substantially higher.

More recent estimates indicate that in 2024:

- 36% of U.S. households had medical debt

- 21% had a past-due medical bill

- 23% were actively paying a medical bill over time to a provider

- 15% were contacted by a third party to collect a medical debt

These figures demonstrate that medical debt is not an isolated event but a recurring financial obligation for a large share of American families.

Medical Debt Persists Despite High Insurance Coverage

Health insurance coverage in the United States exceeds 90% of the population, yet medical debt remains common among insured adults. This disconnect highlights the difference between having coverage and being protected from high out-of-pocket costs.

Adults who were insured for the full year are still likely to report medical debt. Survey data shows:

- 8% of adults insured all year had medical debt

- 14% of adults uninsured for part of the year had medical debt

- 11% of adults uninsured for the entire year had medical debt

High deductibles, copayments, coinsurance, denied claims, and out-of-network charges frequently result in medical bills that insured patients cannot afford. For many households, insurance coverage delays costs rather than eliminating them.

Medical Debt Statistics by Amount

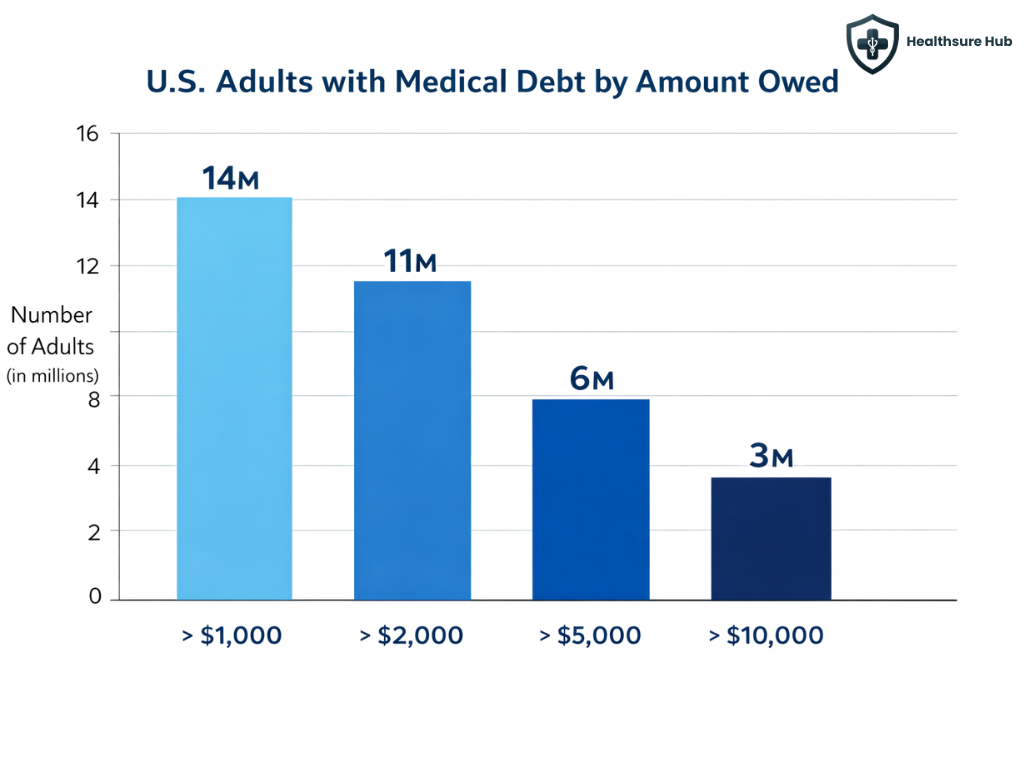

The amount of medical debt owed varies widely, but most people with medical debt owe far more than a few hundred dollars. Among the 20 million adults with medical debt:

- Approximately 14 million people (6% of U.S. adults) owe more than $1,000

- About 11 million owe over $2,000

- Roughly 6 million owe more than $5,000

- Around 3 million adults (1%) owe more than $10,000

While most people with medical debt owe between $1,000 and $5,000, a relatively small group of individuals with very high balances accounts for a disproportionate share of total medical debt nationwide.

Total Medical Debt Statistics in the United States

Estimating total medical debt is challenging because not all debt appears on credit reports. Survey-based estimates consistently show much higher totals than credit bureau data.

Researchers estimate that Americans owed at least $220 billion in medical debt at the end of 2021. This figure reflects unpaid medical bills over $250 per person and excludes extremely high outliers to avoid overestimation.

By comparison, the Consumer Financial Protection Bureau estimates that $88 billion in medical debt appears on U.S. credit reports. The large gap between these figures exists because:

- Not all medical debt is sent to collections

- Some debt is paid using credit cards or personal loans

- Informal borrowing from family and friends is not reported

- Some individuals lack credit reports altogether

Taken together, these estimates suggest that total medical debt is likely far higher than what credit data alone captures.

Who Is Most Likely to Have Medical Debt?

Medical debt affects people across demographics, but certain groups face significantly higher risk.

Health status is one of the strongest predictors of medical debt. Adults who report their health as “fair” or “poor” are far more likely to carry medical debt than those in good or excellent health.

Similarly, adults living with a disability are more than twice as likely to report medical debt:

- 13% of adults with a disability have medical debt

- 6% of adults without a disability have medical debt

Ongoing medical needs, combined with employment disruptions and income loss, often cause bills to accumulate over time.

Medical Debt Statistics by Income Level

Lower-income and middle-income households are disproportionately affected by medical debt, but higher incomes do not eliminate risk.Survey data shows that about 1 in 10 adults with household incomes below 400% of the federal poverty level have medical debt. Also, adults living in poor health with higher incomes are still more likely to have medical debt than healthier adults with lower incomes.

Many insured households lack sufficient savings to cover deductibles or out-of-pocket maximums. In 2019 medical debt statistics show that 32% of single-person insured households with private insurance couldn’t pay a $2,000 bill.

Medical Debt Statistics by Age

Medical debt increases with age until people become eligible for Medicare. Study shows that 12% of adults aged 50–64 report on having significant medical debt compared to 6% of adults ages 65-79.

This pattern reflects higher healthcare use before Medicare coverage begins and gaps in affordability for near-retirees.

Racial and Gender Disparities in Medical Debt

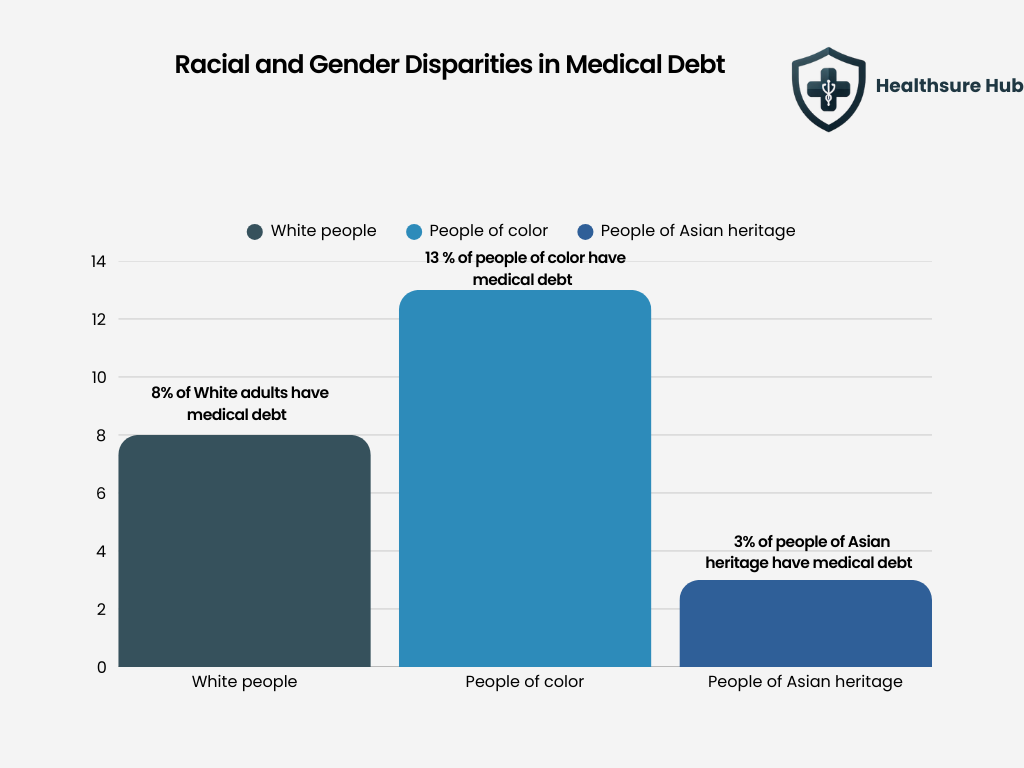

Medical debt statistics reveal significant racial and ethnic disparities. More than 13% of Black adults in the United States report having medical debt, compared with 8% of White adults and just 3% of Asian adults, highlighting a substantial gap in financial exposure to healthcare costs across populations.

Gender-based medical debt statistics indicate higher prevalence among women. About 9% of women have medical debt, compared to 7% of men.

These disparities are linked to income inequality, wealth gaps, differences in insurance coverage, and higher healthcare utilization related to childbirth and caregiving. This gap may partly reflect differences in financial protections, as surveys show that men are more likely than women to hold life insurance, which can provide additional financial resources during health-related expenses.

The Financial Impact of Medical Debt on Households

Medical debt often forces households to make difficult financial tradeoffs. Polling shows that people with medical debt commonly report:

- Cutting spending on food, clothing, or utilities

- Draining savings accounts

- Borrowing from family or friends

- Taking on credit card debt

- Delaying or skipping future medical care

Medical debt is closely linked to broader financial distress and can trap households in long-term cycles of debt and reduced access to care

Hospital Bad Debt and the Provider Impact

When patients cannot pay their bills, hospitals absorb the losses as bad debt. Nationwide:

- Hospitals report over $50 billion in bad debt

- Nearly 30% of hospitals report more than $10 million in bad debt

Large health systems carry billions in unpaid patient balances, while small and rural hospitals face disproportionate financial strain.

Insured Patients Now Drive Most Hospital Bad Debt

High-deductible health plans have shifted bad debt from uninsured patients to insured ones. It is shown that 58% of hospital bad debt now comes from self-pay after insurance, while patient balances over $7,500 have nearly tripled since 2018

As out-of-pocket costs rise, hospitals are increasingly unable to collect even from insured patients.

Emergency Care and Surprise Medical Debt

Emergency situations are a major driver of unexpected medical debt. Patients often:

- Cannot choose providers

- Receive out-of-network services

Face ambulance and facility charges without consent

These scenarios can result in thousands of dollars in medical debt for care patients did not actively choose.

Why Medical Debt Remains a Structural Problem

Medical debt persists not because Americans lack insurance, but because:

- Healthcare prices are high

- Cost-sharing is significant

- Coverage exclusions are common

- Income often drops during illness

Expanding coverage alone does not eliminate medical debt without addressing affordability and financial protection.

Conclusion

Medical debt statistics make clear that tens of millions of Americans are affected, with the burden most concentrated among people in poor health, those with disabilities, lower- and middle-income households, and communities already facing economic disadvantage. These figures highlight that medical debt is not a personal failure, but a systemic issue. Until healthcare costs, insurance design, and income protections are addressed together, medical debt will remain a defining financial challenge for U.S. households.

Sources:

https://www.ama-assn.org/system/files/a24-cms05.pdf

https://www.creditninja.com/blog/percentage-of-americans-have-medical-debt/ https://www.healthsystemtracker.org/brief/the-burden-of-medical-debt-in-the-united-states/ https://www.consumerfinance.gov/about-us/newsroom/cfpb-estimates-88-billion-in-medical-bills-on-credit-reports/

https://www.definitivehc.com/blog/hospital-bad-debt-statistics-you-need-to-know