When your car is damaged in an accident or unexpected event and becomes unusable, the disruption can be stressful and expensive. Loss of use coverage for auto insurance is designed to fill that gap, helping you stay mobile and avoid out-of-pocket transportation costs. Understanding this coverage ensures you are prepared when your vehicle is temporarily out of service.

We explain what is loss of use coverage for auto, how it works, what it covers, limits to be aware of, and why it is an important addition to your auto insurance.

What is Loss of Use Coverage for Auto?

What is loss of use coverage for auto? It’s an optional add-on to your auto insurance, often referred to as rental reimbursement coverage, that pays for substitute transportation when your insured vehicle cannot be used. This often happens due to a covered event, such as a collision, theft, or comprehensive-type damage. Unlike liability coverage, which only covers damages to others, loss of use specifically addresses your own inability to drive your car.

Approximately 16.5 million auto insurance claims are filed annually in the U.S., meaning a large volume of vehicles get damaged each year, often triggering coverage benefits including loss of use.

How Does Loss of Use Coverage for Auto Work?

Understanding what is loss of use coverage for auto helps you plan for rental cars, rideshares, and public transit while your vehicle is being repaired. Typically, you must have collision and comprehensive coverage before you can activate loss of use benefits. Once your vehicle is inoperable, the coverage helps with transportation costs, including rental cars, rideshare, taxi fares, or public transit, depending on your policy. The coverage usually begins the day your vehicle is taken in for repairs and continues until your car is returned, the coverage limit is reached, or in some cases, a total loss settlement is offered.

There’re two ways the claim could go, depending on the circumstances of the claim.

Understanding first-party claims

A first-party claim uses your own collision and loss of use coverage. This is often the quickest way to access transportation when your vehicle is in the shop. Your insurer may pay the rental agency directly, or reimburse you after submitting receipts for taxis, rideshares, or rental fees.

First, if you’re at fault you have to file a claim with the insurance company, then get an estimate at a local mechanic. After deciding on where to leave your car, drop off the vehicle and pick up the rental car. When the car is repaired, or when you reach your coverage limit, you get to return the rental car, whichever comes first.

Knowing your daily and total policy limits is crucial. For example, if your policy provides $50 per day for up to 30 days, and repairs take four weeks, your total coverage would be $1,500 — even if actual transportation costs exceed this. Keeping organized records of rental agreements, receipts, and repair estimates ensures a smooth claims process and prevents delays.

Understanding third-party claims

A third-party claim applies when another driver causes the damage. While you are entitled to compensation for transportation costs from the at-fault driver’s insurer, the process is often slower. The insurance company must investigate the accident, determine fault, and approve reasonable transportation expenses before issuing payment.

Many drivers choose to file a first-party claim first to avoid delays, while their insurer later recovers costs from the at-fault driver’s insurance through subrogation. This ensures immediate mobility without sacrificing your right to full reimbursement.

If you’re not at fault, the process is largely the same, with one key difference: you need to file a claim with the at-fault driver’s insurance company. If they take too long to respond, you should file a claim with your own insurance company and get an estimate from a local mechanic. Be sure to save all receipts and documentation for the repairs, as you’ll need them for reimbursement later.

What Loss of Use Covers

Loss of use coverage focuses on practical transportation solutions. It generally covers:

- Rental car fees, up to daily and total policy limits

- Alternative transportation like Uber, Lyft, taxis, or public transit

When your auto is deemed inoperable, the insurance company provides you with a rental vehicle like the one you had, if the insurance policy covers the same amount. So if your sedan is at the mechanic, the insurance company will fit you with a similar, if not the same, make and model of the car. But be careful, as the insurance company is in a position to deny your claim in case you choose a luxurious rental car over the one being repaired.

This coverage ensures that your daily routine, commuting, errands, or family responsibilities. can continue with minimal disruption while your vehicle is unavailable.

While coverage is robust, it does not pay for fuel, rental insurance add-ons, deposits, or luxury vehicle upgrades beyond your policy’s limit. Being aware of these exclusions helps prevent unexpected expenses.

How State Laws Affect Claims

State regulations can influence how loss of use claims are handled. In no-fault states, your own insurance may cover loss of use regardless of who caused the accident. In other states, eligibility may depend on who is at fault. Understanding local rules and communicating clearly with your claims adjuster helps prevent misunderstandings and ensures you receive the maximum benefit available.

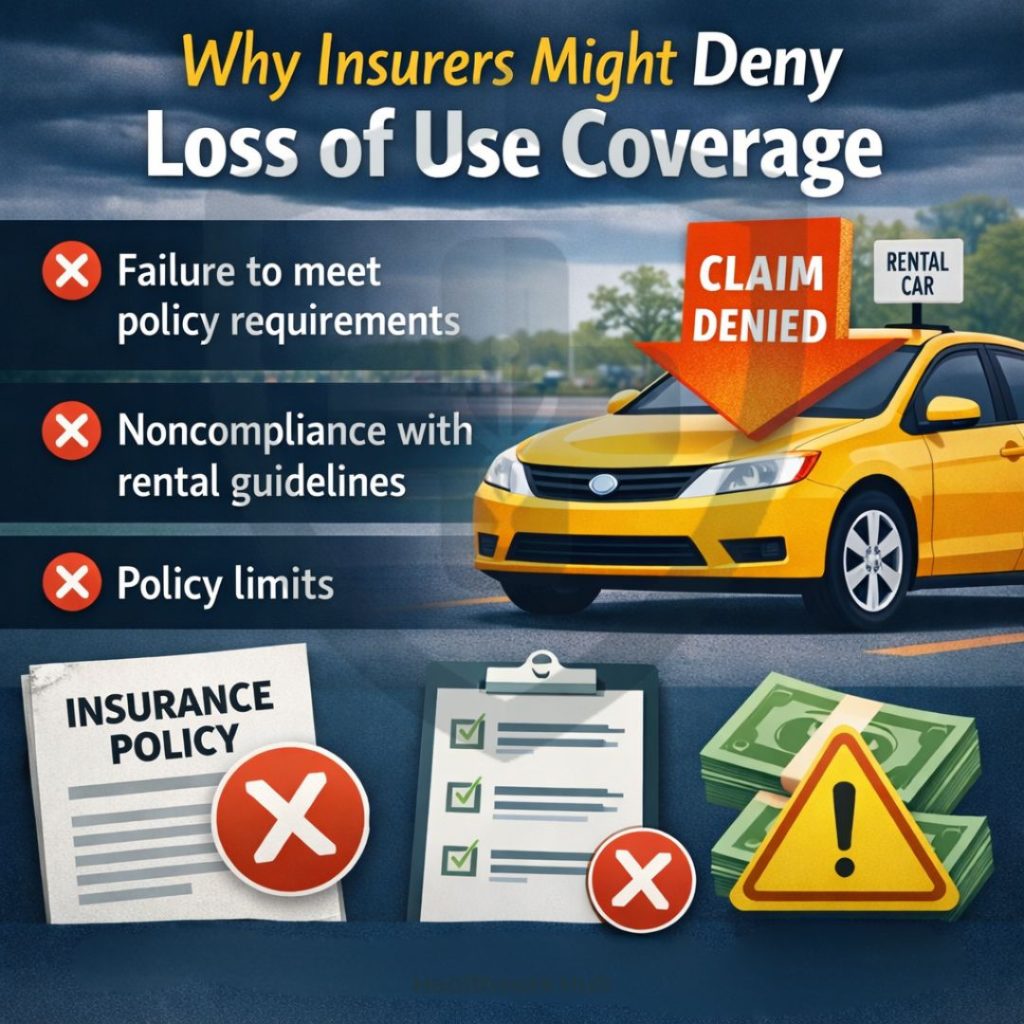

Why Insurers Might Deny Loss of Use Coverage

Even though loss of use coverage is designed to keep you mobile, insurers sometimes deny claims or reduce payments.

Failure to meet policy requirements

One common reason is failure to meet policy requirements. For example, loss of use coverage typically only applies if your car is damaged in a covered incident, such as a collision or comprehensive loss. If the insurer believes the damage was not covered, or that repairs were unnecessary, they may deny the claim.

Noncompliance with rental guidelines

Another reason is noncompliance with rental guidelines. Insurers often require that the substitute vehicle be of comparable size and type to your insured car. Choosing a luxury sports car instead of a mid-size sedan may result in claim denial. Similarly, some policies require using an approved rental agency or obtaining prior approval before renting; skipping these steps can trigger denials.

Policy limits

Policy limits are also a factor. If your claim exceeds your daily or total loss of use limits, the insurer will not cover the extra cost. For example, if your policy caps coverage at $50 per day and $1,500 total, but your rental costs are higher, you are responsible for the difference.

Other reasons include:

- Delays caused by the policyholder in bringing the car to a repair shop

- Lack of documentation, such as repair estimates or rental receipts

- Insufficient proof of dependency on the vehicle, especially if the insurer doubts that transportation is essential for daily life

By knowing these potential pitfalls in advance, you can take proactive steps, such as keeping detailed records, coordinating with the repair shop, and choosing appropriate rentals, to maximize your chances of approval.

Tips for Maximizing Your Claim

- Submit organized documentation, including receipts and repair estimates.

- Understand your daily and total policy limits.

- Communicate promptly with your adjuster about your transportation needs.

- Consider filing first-party claims for speed, then allow subrogation if the other driver is at fault.

By following these practices, loss of use coverage becomes a reliable safety net, keeping your life moving while your car is being repaired or replaced.

Costs and Limitations of Loss of Use Coverage

Knowing what is loss of use coverage for auto and its limitations ensures you choose the right daily and total reimbursement amounts for your needs. While loss of use coverage is valuable, it is not free and comes with limitations that vary by insurer and policy. The cost is generally modest, often ranging from $2 to $15 per month, depending on factors such as vehicle type, coverage limits, and state regulations.

Most policies impose daily limits on how much they will reimburse for substitute transportation. Common ranges are $25 to $70 per day, though some policies offer higher amounts for luxury or specialty vehicles. Additionally, there is usually a total claim limit, which might range from $900 to $1,500, meaning the insurer will only cover transportation for a set number of days.

Other limitations to consider include:

- Exclusions for fuel, insurance on the rental, or deposits

- Restrictions on vehicle type or rental company, sometimes requiring use of an approved vendor

- Driver eligibility rules, such as minimum age requirements or license validity, which can affect rental approvals

- Total loss scenarios, where some insurers may only offer interim transportation reimbursement until settlement funds are released

Despite these limits, loss of use coverage often proves highly cost-effective. Paying a small monthly premium protects you from potentially hundreds of dollars in out-of-pocket transportation costs while your car is unavailable. Evaluating your driving needs, local rental costs, and policy limits ensures that the coverage aligns with your lifestyle and offers real peace of mind.

Conclusion

In short, understanding what is loss of use coverage for auto provides peace of mind and keeps you mobile while your car is being repaired or replaced. It covers rental cars, rideshares, and other transportation costs, helping you avoid out-of-pocket expenses. Understanding how it works, its limits, and claim process ensures peace of mind. Even with modest premiums, this coverage provides practical protection, making daily life and commuting easier while your car is being repaired