Imagine you sign up for a new health insurance plan thinking the $150 monthly premium is affordable, only to face a $3,000 deductible after a single medical procedure. Suddenly, that “budget-friendly” plan isn’t so cheap after all. How do these two costs really interact, and what’s the smartest balance for your financial situation?

Understanding the interplay between insurance premium vs deductible can save you money, reduce stress, and help you make confident decisions about your coverage.

Insurance Premium vs Deductible

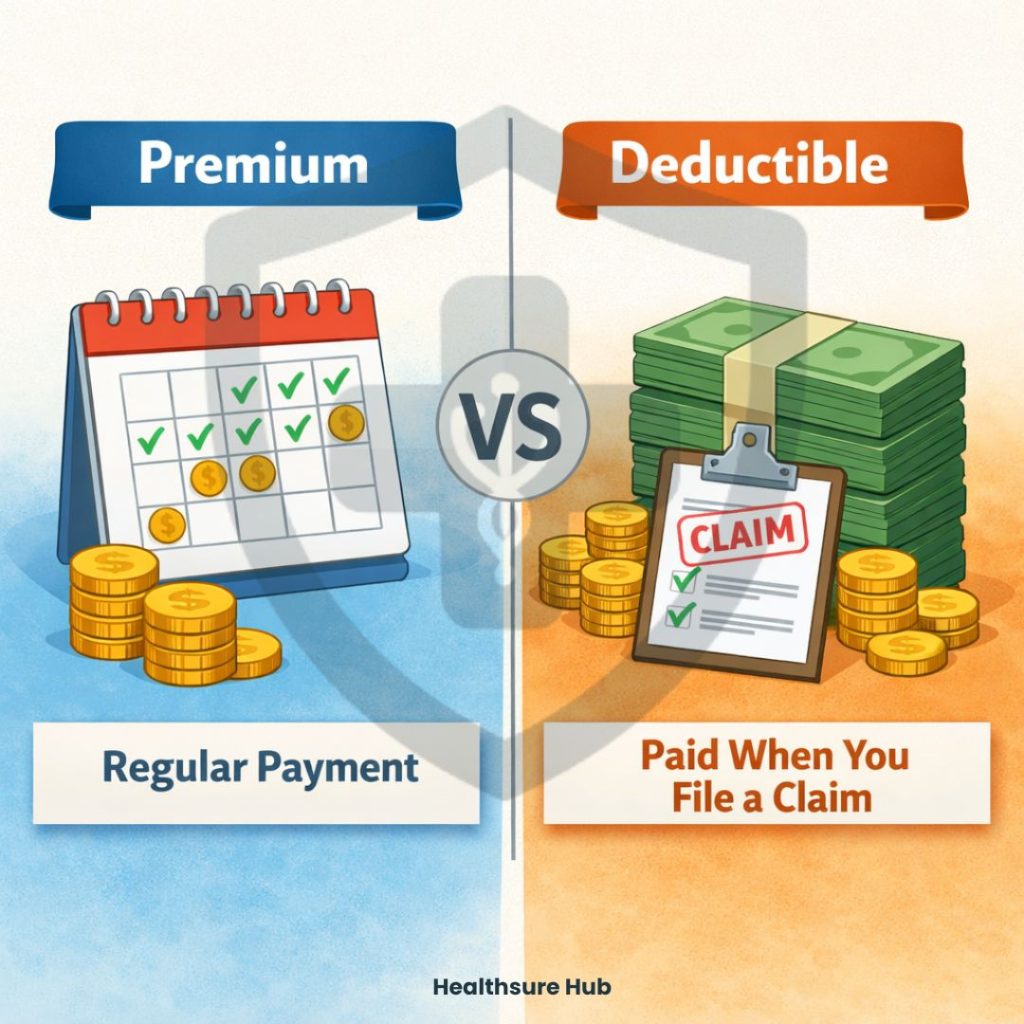

At its core, the difference between insurance premium vs deductible is about timing and risk. A premium is the regular payment you make to keep your insurance policy active, whether monthly, quarterly, or annually. It’s the predictable cost you pay to maintain protection, even if you never file a claim.

A deductible, on the other hand, is the amount you must pay out of your own pocket before your insurance begins to cover a claim. In essence, the deductible is the cost you bear when something goes wrong, while the premium is the cost you bear simply to maintain coverage.

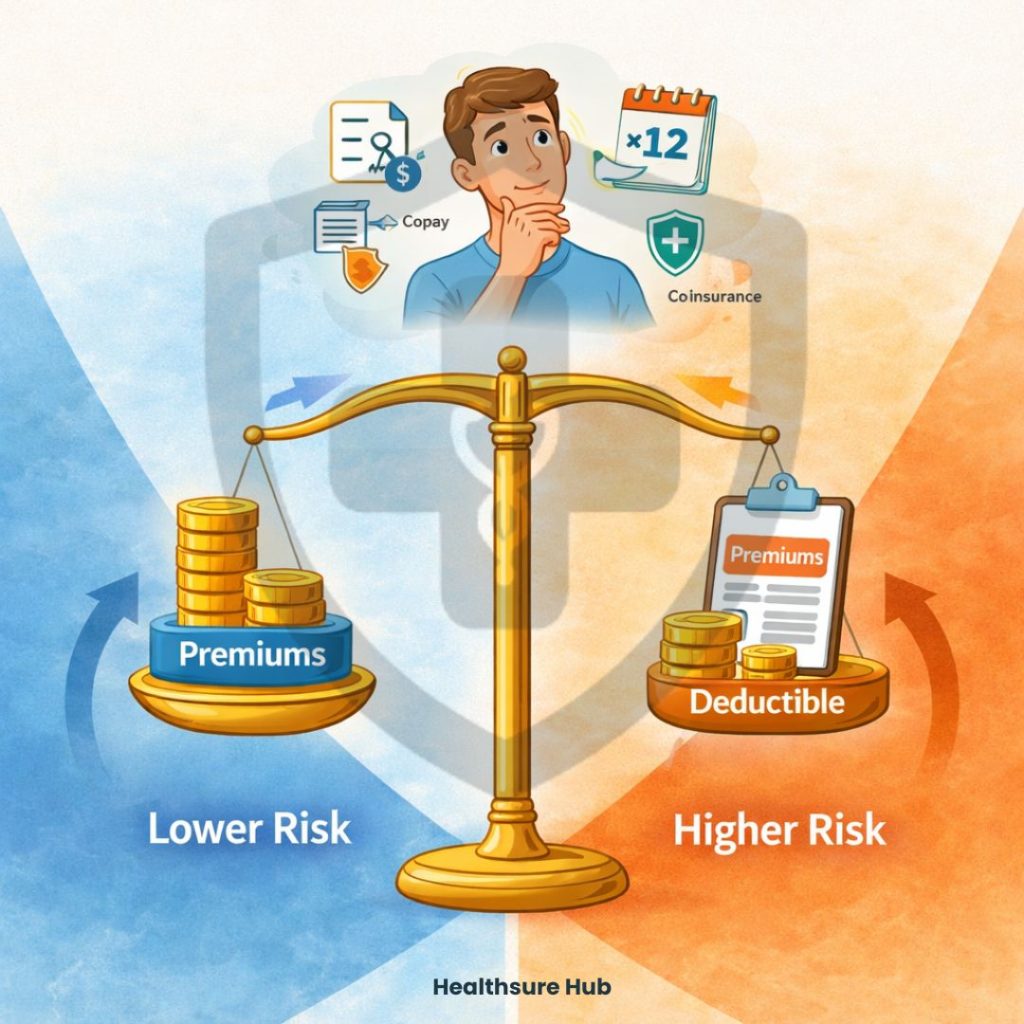

Typically, a higher deductible results in a lower premium, and vice versa. This inverse relationship between insurance premium vs deductible is a fundamental concept in understanding insurance costs.

| Feature | Premium | Deductible |

| Definition | Regular payment to maintain coverage | Out-of-pocket cost before insurance pays |

| When You Pay | Monthly, quarterly, annually | When filing a claim |

| Cost Type | Predictable, ongoing | Variable, claim-triggered |

| Risk Level | Low, predictable | Higher, risk borne by policyholder |

| Best For | Peace of mind, predictable budgeting | Individuals willing to take on some risk for lower monthly payment |

What Is an Insurance Premium?

An insurance premium is the price you pay to maintain your policy, whether it’s for health, auto, homeowners insurance, or business coverage. Premiums are typically collected on a recurring schedule, monthly, quarterly, or annually, and failing to pay them can result in the cancellation of your coverage.

Premium amounts are not arbitrary; they are carefully calculated by insurance underwriters based on a variety of factors, such as:

- Your risk profile, including your age, health, or driving record, plays a major role.

- The type and level of coverage, the location of the insured property, and your claims history also influence the premium.

For example, a young driver purchasing auto insurance will often face higher premiums than an experienced driver because statistics show higher accident rates among younger motorists. Similarly, a family health plan covering multiple dependents will naturally have a higher premium than an individual plan, reflecting the increased risk the insurer assumes.

Understanding what drives your premium is essential to understand the difference between insurance premium vs deductible, because it represents the predictable portion of your insurance budget, allowing you to plan financially year-round.

What Is Deductible?

When talking between insurance premium vs deductible, a deductible is the portion of a claim you must pay out of pocket before your insurance coverage takes over. Deductibles can vary in type and structure depending on the type of insurance:

- Flat or fixed deductibles– A set dollar amount you pay per claim or per policy year.

- Percentage deductibles– Often used in property insurance, calculated as a percentage of the insured value.

- Per-claim vs. annual deductibles– Common in health and auto insurance, either per event or reset annually.

Deductibles reset at the beginning of each policy year, meaning you must meet the amount again before your insurance starts paying.

For example, if your auto insurance policy has a $500 deductible and you experience a $2,000 accident, you pay $500 and your insurer covers the remaining $1,500. In health insurance, a $1,500 deductible for a knee surgery means you pay the first $1,500 before your coverage takes over, potentially combined with coinsurance or copayments.

How Insurance Premium vs Deductible Work Together

Premiums and deductibles share a balancing act that affects your total costs. Higher premiums usually come with lower deductibles, offering more predictable coverage. Lower premiums often pair with higher deductibles, giving you savings upfront but higher potential out-of-pocket costs when a claim occurs.

Think of it as a see-saw: the more you pay regularly, the less you pay when something goes wrong. The less you pay regularly, the more financial risk you shoulder when claims arise. This relationship is fundamental to choosing a plan that fits both your health or property needs and your budget.

A common misconception is that the premium contributes to the deductible. It does not. The premium is a fixed, recurring payment, whereas the deductible is claim-triggered. Understanding this prevents surprises, as low monthly premiums do not reduce the amount you pay out-of-pocket before insurance coverage begins.

Which Is Better, Higher Premium or Higher Deductible?

There isn’t a single answer that works for everyone when considering insurance premium vs deductible; the best choice depends on your personal or family circumstances. A higher deductible can be ideal for generally healthy individuals or families who have a cushion of emergency savings and rarely file claims.

With this approach, your monthly premiums are lower, but you take on more financial risk when unexpected events occur. On the other hand, a lower deductible may be better for those who have chronic conditions, frequent medical needs, or simply prefer predictable costs. While monthly premiums are higher in this scenario, your out-of-pocket expenses when filing a claim are significantly reduced. Ultimately, making the right decision requires thoughtful consideration of your risk tolerance, budget, and lifestyle, ensuring that the plan you choose balances affordability with financial security.

How to Choose the Right Balance

Selecting the optimal plan requires evaluating both affordability and risk exposure. When making a decision between insurance premium vs deductible first, ensure your deductible is an amount you could comfortably pay if necessary. Next, consider the total annual cost, including premiums, potential deductibles, and additional out-of-pocket expenses like copays and coinsurance.

A practical step is to run a mental cost calculation: multiply your monthly premium by 12, add the deductible, and estimate your expected annual medical or insurance usage. This exercise highlights which balance offers the most cost-effective coverage.

Common Mistakes Between Insurance Premium vs Deductible

Even experienced policyholders often make errors when choosing between insurance premium vs deductible. One common mistake is focusing solely on the lowest monthly premium without considering whether the deductible is affordable in the event of a claim.

Some also overlook the total out-of-pocket costs, including copays and coinsurance, which can quickly accumulate during the year. Others underestimate their annual expenses or fail to account for how frequently they might need to use insurance. For example, real-world data on homeowners insurance claims shows how often policyholders face unexpected costs and claim events, which highlights why understanding deductibles is so important. Misunderstanding these dynamics can lead to unpleasant financial surprises.

How Premium vs Deductible Works Across Insurance Types

The relationship between insurance premium vs deductible applies across all types of insurance, though the details vary by policy. In auto insurance, per-claim deductibles determine how much you pay out-of-pocket for each accident, while in health insurance, annual deductibles reset each year and combine with coinsurance and copays to determine your total costs.

Homeowners insurance may use a flat deductible or a percentage of the property value, impacting claims differently depending on the size of damage. Business insurance offers adjustable deductibles and coverage limits that reflect industry risks and operational exposure. Understanding these differences between insurance premium vs deductible allows you to tailor your coverage to your specific risk profile, ensuring that you balance affordability with protection across every type of policy.

Conclusion

Insurance premiums are predictable, ongoing payments, whereas deductibles represent the risk you bear when a claim occurs. These two costs share an inverse relationship: as premiums go up, deductibles typically go down, and vice versa. Determining the right balance depends on your financial situation, risk tolerance, and expected insurance usage. To make informed decisions, it’s important to calculate the total cost of coverage, including premiums, deductibles, copays, and coinsurance. By understanding the dynamics between insurance premium vs deductible, you can confidently select coverage that protects your finances while maximizing the value of your insurance policy.