Insurance fraud remains one of the most costly and complex forms of financial crime in the United States. In 2025, insurance fraud statistics show that fraud continues to affect every line of insurance—from auto and health to property and life—driving up premiums for honest policyholders and challenging insurers and law enforcement alike.

Our team at HealthSure Hub analyzed the latest industry reports, government enforcement data, and insurer studies to present the most up-to-date insurance fraud statistics, emerging trends, and financial impacts shaping the U.S. insurance market today.

What Is Insurance Fraud?

Insurance fraud occurs when an individual or organization intentionally misrepresents facts to obtain financial gain from an insurance policy. As reflected in national insurance fraud statistics, it can happen at multiple stages:

- Application fraud (lying to get a lower premium)

- Claims fraud (filing false or exaggerated claims)

- Provider fraud (billing for unnecessary or nonexistent services)

- Organized schemes involving identity theft or synthetic identities

Fraud schemes range from soft fraud (exaggerating a legitimate claim) to hard fraud (deliberately staging accidents or damage). These activities undermine the integrity of the insurance system and directly increase costs for consumers. Industry insurance fraud statistics estimate that over 10% of all insurance claims contain some element of fraud, whether exaggerated, misrepresented, or entirely fabricated.

Insurance Fraud Fast Facts

Based on leading insurance fraud statistics and industry sources:

- According to the Coalition Against Insurance Fraud. U.S. insurance fraud exceeds $308.6 billion each year.

- Global losses are estimated at over $1 trillion annually.

- Between 1 in 50 and 1 in 10 insurance claims show signs of fraud

- National Health Care Anti-Fraud Association (NHCAA) estimates tens of billions in annual losses due to healthcare fraud.

- Fraud detection technology spending continues to rise as insurers face increasingly complex schemes.

Insurance Fraud by State

Top 10 States for Insurance Fraud Risk (2025)

| Rank | State | Risk Level |

|---|---|---|

| 1 | Georgia | Very High |

| 2 | Florida | Very High |

| 3 | Delaware | Very High |

| 4 | Nevada | High |

| 5 | Maryland | High |

| 6 | New Jersey | High |

| 7 | New York | High |

| 8 | California | High |

| 9 | Louisiana | High |

| 10 | Texas | Moderate |

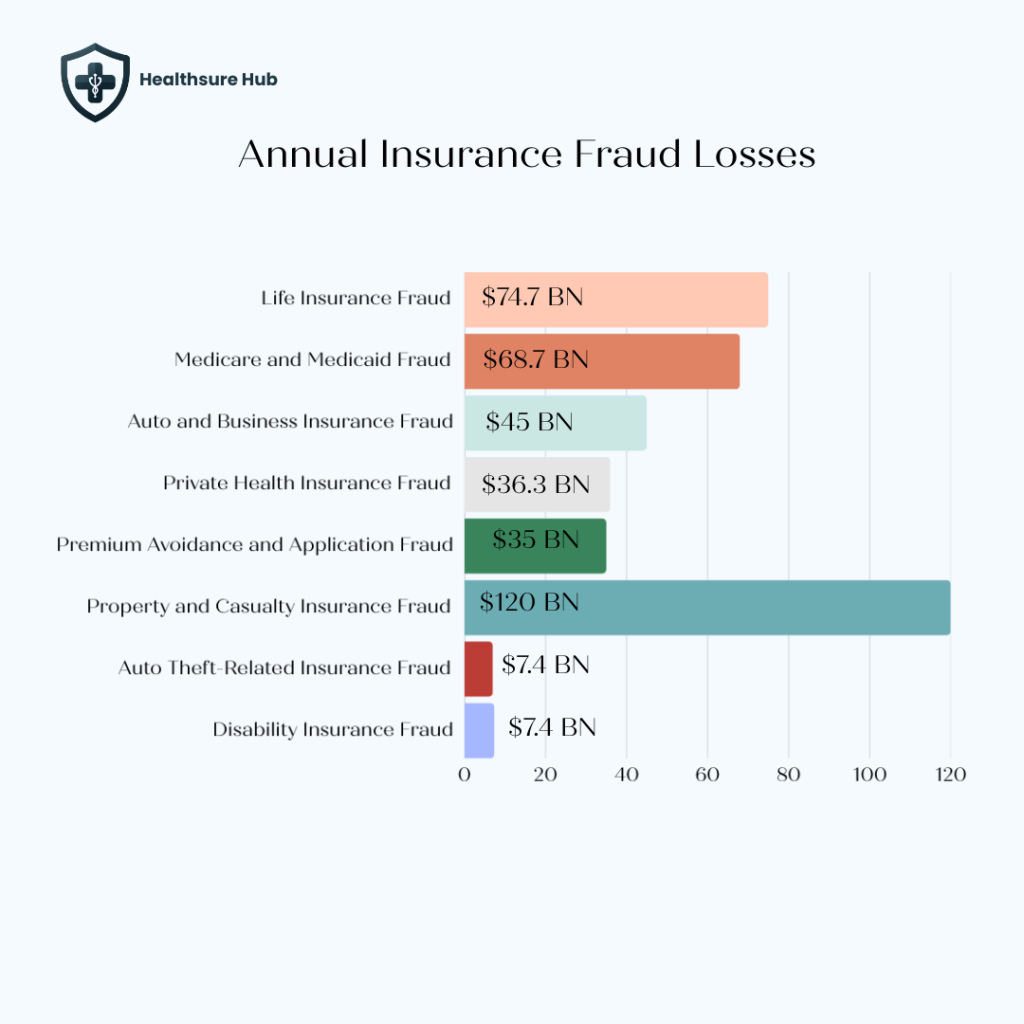

Annual Insurance Fraud Losses by Category

Leading insurance fraud statistics estimate annual losses as follows:

- Life insurance fraud: $74.7 billion

- Medicare and Medicaid fraud: $68.7 billion

- Auto, and business insurance fraud: $45 billion

- Private health insurance fraud: $36.3 billion

- Premium avoidance and application fraud: $35.1 billion

- Workers’ compensation fraud: $34 billion

- Property and casualty: $90- 120 billion

- Auto theft-related insurance fraud: $7.4 billion

- Disability insurance fraud: $7.4 billion

Life insurance fraud represents the single largest category, accounting for nearly one-quarter of all insurance fraud losses.

Auto Insurance Fraud Statistics

Auto insurance fraud remains one of the most widespread and expensive forms of fraud according to national insurance fraud statistics.

- Auto insurers lose tens of billions of dollars annually due to fraud.

- Lost premiums from application fraud alone account for approximately $29 billion per year.

- Up to 14% of every auto insurance premium dollar goes toward covering fraud-related losses.

Common Sources of Auto Insurance Fraud Losses

As reflected in insurance fraud statistics, common sources include failing to list household drivers, underreporting mileage, misrepresenting garaging location, and concealing prior accidents or violations.

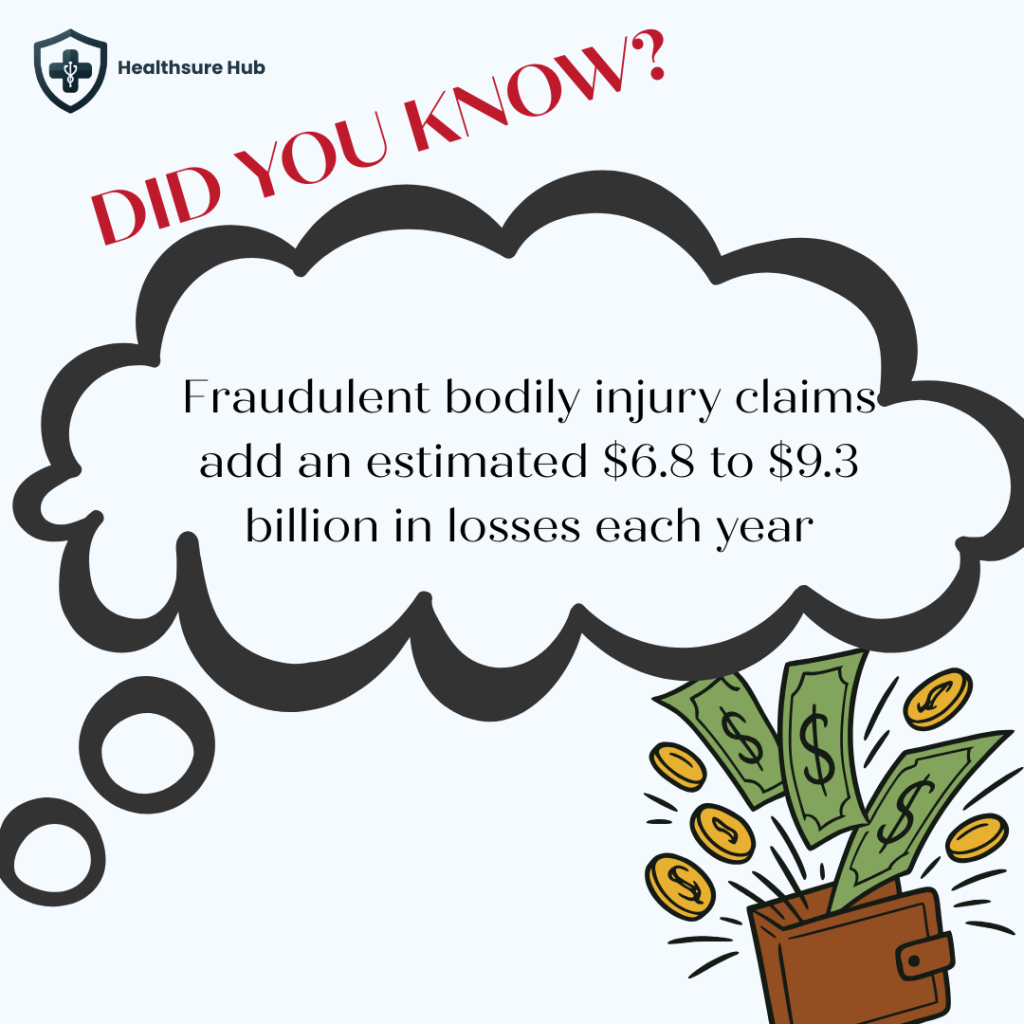

Beyond application fraud, fraudulent bodily injury claims add an estimated $6.8 to $9.3 billion in losses each year, with soft-tissue injuries—such as neck and back pain—being the most frequently exaggerated due to the lack of objective medical evidence and the difficulty insurers face when disputing these claims.

Home Insurance Fraud Statistics

Home insurance fraud is when someone intentionally devices an insurer for some kind of financial gain. Most commonly it involves the policyholder doing intentional damage, inflated repair estimates, or false claims. A perfect example is when a failing business owner burns down its store to gain money from the insurance company in order to gain the lost money back. While this is intentional, some claims are more subtle like a burglary. While the burglary did happen, the houseowner claims that some valuable items are stolen in order to get the money’s value of the belongings, while in fact they were not stolen or didn’t exist in the first place.

Fraud spikes significantly following natural disasters, when claim volumes surge and oversight is strained. After Hurricanes Katrina and Rita that took the U.S. ground by storm in 20025, insurance fraud statistics from the U.S. Government Accountability Office found over $20 million in potentially improper or fraudulent payments to individuals who have used the same property registered for assistance for both hurricanes.

Common home insurance fraud schemes include:

- Exaggerating storm or fire damage

- Claiming pre-existing damage as a covered loss

- Inflating the value of stolen items

- Contractor-driven fraud involving padded repair estimates

Life Insurance Fraud Statistics

Life insurance fraud is the largest single contributor to losses based on insurance fraud statistics, costing insurers an estimated $74.7 billion annually. Unlike auto or property fraud, life insurance fraud often goes undetected for years, allowing losses to compound before a claim is ever reviewed.

This form of fraud occurs at multiple stages of the policy lifecycle and involves a wide range of actors. This category includes fraud committed by:

- Applicants who misrepresent health, age, or income

- Policyholders who conceal material information

- Beneficiaries who manipulate policy ownership or claims

- Industry insiders who divert premiums or sell fake policies

Types of Life Insurance Fraud

Application fraud is one of the most common entry points. For example, an applicant may fail to disclose a history of heart disease, cancer treatment, or smoking in order to qualify for lower premiums or higher coverage limits. In other cases, individuals understate their age or inflate income to justify larger policy values. These misrepresentations often surface only after death, when insurers review medical records during the claims process.

Policyholder fraud can involve concealing material changes after a policy is issued. A policyholder might take up high-risk activities such as extreme sports or hazardous occupations without notifying the insurer, despite policy terms requiring disclosure. When a claim is filed years later, these omissions can significantly alter the insurer’s risk exposure.

Beneficiary fraud frequently centers on manipulation of policy ownership or claims. Real-world cases include forged beneficiary change forms submitted shortly before the insured’s death, or beneficiaries attempting to collect proceeds for individuals who are still alive or never existed. In rare but documented cases, beneficiaries have even been involved in intentionally causing the policyholder’s death to trigger a payout.

Insider and agent-driven fraud represents another costly segment. Unscrupulous agents have been caught collecting premiums without remitting them to insurers, selling counterfeit policies, or diverting legitimate payments for personal use. These schemes often affect multiple policyholders simultaneously and can remain hidden until claims are denied.

As shown in long-term insurance fraud statistics, these schemes can remain hidden for decades, increasing financial exposure when claims are finally reviewed

Health Insurance, Medicare, and Medicaid Fraud Statistics

Combined public and private health insurance fraud statistics account for more than one-third of total insurance fraud losses:

- Private health insurance fraud: $36.3 billion annually

- Medicare and Medicaid fraud: $68.7 billion annually

Medicare and Medicaid recipients are especially vulnerable due to age, disability, and the complexity of medical billing. The 2025 National Health Care Fraud Takedown resulted in 324 defendants charged in schemes involving more than $14.6 billion in alleged improper claims.

Fraud in these programs is often driven by providers rather than patients. Fraud in Medicare and Medicaid is more present than with private health insurance. This is due to the fact that the recipients in these healthcare companies are older or disabled. Plus, the people receiving Medicaid pay little to no money for medical care so they’re less likely to notice if they get charged for extra treatments.

Common health insurance fraud schemes include:

- Billing for services never rendered

- Upcoding and unbundling procedures

- Falsifying diagnoses to justify unnecessary care

- Identity theft and benefit misuse

Trends Driving Insurance Fraud in 2025

Rise of Identity Theft and Synthetic Identities

According to the National Insurance Crime Bureau (NICB) insurance fraud statistics, identity-related insurance fraud is projected to rise nearly 49% in 2025. This includes fraud involving both traditional identity theft and synthetic identities (fake identities built using real and fabricated information). These techniques are often used in:

- Life insurance scams

- Healthcare billing fraud

- False claims filed under stolen identities

Technology: Both a Risk and a Solution

Advancements in artificial intelligence and predictive analytics are reshaping the fraud landscape. While fraudsters increasingly use technology to create convincing fake evidence and identities, insurance fraud statistics found that insurers are also deploying AI-based systems to detect suspicious patterns more effectively.

The U.S. Department of the Treasury announced that AI-powered fraud detection prevented an estimated $1 billion in fraudulent activity in 2024, representing a substantial uplift in detection capability.

Insurance Fraud Enforcement and Detection Trends

Insurance fraud is classified as a felony in most U.S. states, carrying penalties that may include fines, restitution, and prison sentences. Every state maintains some form of insurance fraud enforcement or investigation unit.

Insurers increasingly rely on advanced analytics, predictive modeling, and artificial intelligence to detect fraud earlier in the claims process. Industry surveys show that over 80% of insurers now use predictive modeling tools, up significantly from pre-pandemic levels.

Despite these advances, globalized and digitally enabled fraud remains a growing concern, with many insurers reporting limited confidence in their ability to combat cross-border fraud networks.

Conclusion

Insurance fraud statistics clearly demonstrate that fraud is not a victimless crime—it is a systemic financial drain that ultimately impacts every household in the United States. As the data shows, fraud now costs the industry hundreds of billions of dollars each year, spanning auto, health, property, life, and public insurance programs. These losses are not absorbed quietly by insurers; they are passed on through higher premiums, stricter underwriting, reduced coverage options, and increased scrutiny for honest policyholders.

In 2025, insurance fraud statistics show that fraud has become more sophisticated, more organized, and more technology-driven. Identity theft, synthetic identities, provider-led healthcare schemes, and long-tail life insurance fraud illustrate how criminals exploit complexity, volume, and delayed detection. At the same time, natural disasters, aging populations, and strained public programs continue to create environments where fraud can flourish if oversight weakens.

Sources:

https://wallethub.com/edu/states-where-identity-theft-and-fraud-are-worst/17549

https://www.shift-technology.com/resources/reports-and-insights/modernize-fraud-detection

https://hsrc.himmelfarb.gwu.edu

https://web.theinstitutes.org/blog/ai-fraud-auto-claims-now-time-bold-collaboration

https://www.ncdoi.gov/blog/2025/10/22/health-insurance-fraud-makes-premiums-more-expensive

https://www.celent.com/en/insights/551788580

https://www.shift-technology.com/resources/reports-and-insights/modernize-fraud-detection

https://www.valuepenguin.com/auto-home-insurance-fraud#type

https://www.govinfo.gov/content/pkg/GAOREPORTS-GAO-07-300/html/GAOREPORTS-GAO-07-300.htm

https://www.nhcaa.org/tools-insights/about-health-care-fraud/the-challenge-of-health-care-fraud/

https://insurancenewsnet.com/innarticle/the-rising-tide-of-insurance-fraud-an-estimated-308b-problem