Most drivers feel confident once they buy a policy, yet the smartest policyholders know that learning what does auto insurance not cover is even more valuable than knowing what it does. A single overlooked exclusion can turn a covered accident into a denied claim, leaving you responsible for thousands of dollars. Here, we explain every major exclusion, why they exist, and how to avoid costly surprises so you can make confident, informed coverage decisions.

What Does Auto Insurance Not Cover?

Auto insurance does not cover losses that fall outside your policy’s listed protections, including intentional damage, normal wear and tear, business use, unlisted drivers, and mechanical failure. Policies only pay for risks specifically named as covered events.

In simple terms, if a situation is excluded, limited, or conditional in your policy, your insurer will not pay for it. Common exclusions include:

- Intentional damage

- Mechanical breakdown

- Commercial driving

- Personal belongings in the car

- Racing or illegal activity

Why Auto Insurance Policies Exclude Certain Risks

Understanding what does auto insurance not cover becomes easier when you see how insurers design policies. Insurance companies calculate premiums using actuarial risk models that estimate how likely a claim is and how expensive it could be. High-risk or unpredictable situations are excluded so premiums remain affordable for most drivers.

Exclusions differ from limitations and conditions. An exclusion removes coverage entirely. A limitation caps how much the insurer pays. A policy condition requires you to meet certain rules before coverage applies. Regulators such as the National Association of Insurance Commissioners require insurers to clearly list exclusions so consumers understand exactly what protection they are buying. This transparency helps drivers compare policies confidently and choose coverage that fits their needs.

Driver Situations That Auto Insurance Does Not Cover

Many of the most important answers to what does auto insurance not cover involve who is driving. Policies are built around approved drivers and legal operation of the vehicle.

If someone living in your household is not listed on your policy and causes an accident, your insurer may deny the claim because that person represents an undisclosed risk. Driving with a suspended or invalid license can also void coverage instantly because insurers only cover legally permitted drivers. Claims related to driving under the influence are often denied as well, since impaired driving dramatically increases risk and violates policy conditions.

Intentional damage is always excluded. Insurance protects against accidents, not deliberate actions. If someone damages a vehicle on purpose or stages a loss, insurers classify it as fraud and refuse payment.

Vehicle Problems Auto Insurance Will Not Pay For

Auto insurance protects against sudden and accidental loss, not gradual deterioration. Wear and tear, including aging tires, worn brake pads, fading paint, or battery decline, falls under routine maintenance and is never covered. Mechanical failure is also excluded unless it directly results from a covered accident. For example, if an engine fails due to age, insurance will not pay; if it fails because of a collision, it may be covered.

Pre-existing damage is another common exclusion. Insurers only pay for new damage that occurs after the policy begins. Manufacturer defects are also excluded because they fall under warranties or recalls rather than insurance protection.

Uses of a Vehicle That Insurance Will Not Cover

Personal auto policies are designed for private driving, not commercial activity.

If you use your car for business tasks such as deliveries, transporting tools, or client visits, a standard auto insurance policy may deny claims. Driving for rideshare platforms like Uber or Lyft often requires special endorsements because the risk level increases while carrying passengers for profit. Racing, stunt driving, or speed contests are also excluded because they present extreme risk beyond standard policy assumptions.

Property and Financial Losses Not Covered by Auto Insurance

Another important part of learning what does auto insurance not cover involves money and personal property. Standard policies protect the vehicle itself, not everything inside it.

If personal items such as laptops, bags, or electronics are stolen from your car, auto insurance typically will not reimburse you. Those losses usually fall under homeowners or renters insurance instead. Custom modifications can also exceed policy limits. Many insurers cap coverage for aftermarket upgrades unless you purchase additional protection.

Financial gaps can arise after a total loss. Insurance usually pays the vehicle’s actual cash value, which accounts for depreciation. If your loan balance exceeds that value, you must pay the difference unless you carry gap coverage.

If you are in a good financial situation, you may consider putting a higher auto insurance limit or add an umbrella policy for further protection.

Environmental and Situational Events That Are Excluded

While comprehensive coverage protects against many natural events, policies may exclude certain extreme risks depending on region and provider.

Events such as war, nuclear hazards, or government seizure are almost universally excluded because they create catastrophic losses that private insurers cannot reasonably price. Some policies also restrict coverage when driving outside approved geographic territories. Transporting hazardous materials without proper commercial coverage can also void protection because it introduces specialized risks.

Situations That Can Void Coverage Completely

Some actions do not just limit coverage; they cancel it. Providing false information when applying for a policy can lead to denial of all claims because insurers rely on accurate data to set premiums. Missing payments can cause a lapse in coverage, meaning any accident during that time is uninsured.

Failing to disclose regular drivers or major vehicle modifications can also void claims. Insurers price policies based on risk factors such as driver history and vehicle value. When those details change without notice, the policy may no longer apply.

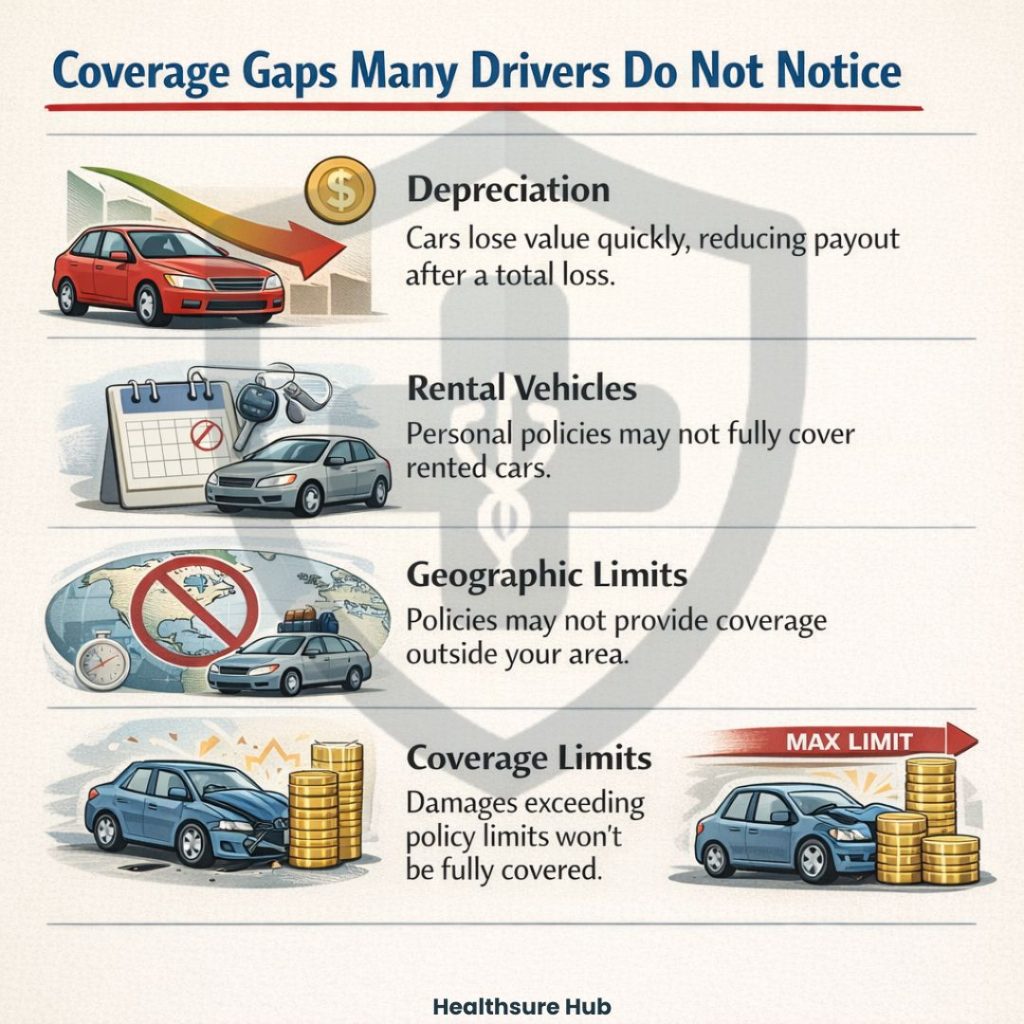

Coverage Gaps Many Drivers Do Not Notice

Even careful drivers sometimes overlook hidden gaps related to what does auto insurance not cover. Depreciation is one of the most common. New vehicles can lose significant value within the first year, which means a payout after a total loss may be less than expected.

Rental vehicles create another gap. A personal policy may not automatically cover rentals unless it extends to temporary substitute vehicles. Geographic limits can also apply, especially for international travel. Coverage limits themselves can create gaps if damages exceed the maximum payout listed in your policy.

Exclusions vs Add-Ons That Solve Them

| Not Covered | Reason | Coverage Solution |

| Loan balance above car value | Depreciation | Gap insurance |

| Rideshare driving | Commercial risk | Rideshare endorsement |

| Custom parts | Value limit | Equipment rider |

| Rental cars | Not automatically insured | Rental coverage add-on |

This comparison shows that many exclusions are manageable once you understand them. Instead of viewing exclusions negatively, informed drivers use them to customize smarter protection.

How to Check What Your Policy Specifically Excludes

The most reliable way to confirm what does auto insurance not cover in your policy is to read the exclusions section of your contract. Look for headings labeled “Exclusions,” “Limitations,” or “Conditions.” These sections clearly list situations where claims will not be paid.

You can also ask your insurer direct questions, such as whether your policy covers other drivers, aftermarket upgrades, or out-of-state travel. Major insurers like GEICO and Progressive provide policy summaries that highlight exclusions in plain language, which makes reviewing coverage much easier. Checking your policy once a year ensures it still matches your lifestyle and driving habits.

Expert Insights That Help You Avoid Coverage Surprises

Drivers who fully understand what does auto insurance not cover consistently experience fewer claim issues. Matching coverage to your lifestyle is one of the most effective strategies. If you start commuting farther, using your vehicle for work, or adding new drivers, updating your policy keeps protection aligned with your risk level.

Increasing liability limits can also strengthen financial protection because serious accidents can exceed minimum coverage requirements. Keeping receipts and photos of vehicle upgrades ensures you can prove their value if you add specialized coverage. These proactive steps transform insurance from a basic requirement into a powerful financial safeguard.

Conclusion

Understanding what does auto insurance not cover becomes simple when you remember three categories. Policies usually cover accidents, theft, and liability events listed in your contract. They do not cover maintenance, intentional acts, or unauthorized use. They require add-ons for special risks such as rideshare driving or loan balance protection. Keeping these distinctions in mind helps you evaluate any policy quickly and confidently.