Umbrella insurance is a powerful financial safety net that protects you when your standard insurance policies, like auto or homeowners insurance, reach their limits. In simple terms, it provides extra liability coverage to safeguard your assets, future income, and personal wealth against unexpected lawsuits or damages. Understanding what does umbrella insurance cover helps you make informed decisions and ensures you are protected against high-cost risks.

What Is Umbrella Insurance?

Umbrella insurance is a type of personal liability insurance designed to provide coverage beyond the limits of your existing policies, including homeowners or dwelling insurance, auto, renters, or boat insurance. Its primary purpose is to serve as an additional layer of protection, stepping in when the liability limits of your primary policies are exhausted.

While most people focus on their auto or homeowners policies, the reality is that the U.S. property and casualty insurance market continues to grow rapidly, with insurers writing about $1.05 trillion in direct premiums in 2024, an 8% increase from the previous year. This growth highlights the rising costs and frequency of claims, making extra liability coverage more important than ever. With an umbrella policy, you can safeguard your assets and avoid paying out-of-pocket for lawsuits or major accidents that exceed your primary policy limits.

By extending the liability coverage of underlying policies, umbrella insurance protects you and your family from catastrophic financial losses. It is not a replacement for standard insurance but a complementary layer that provides peace of mind.

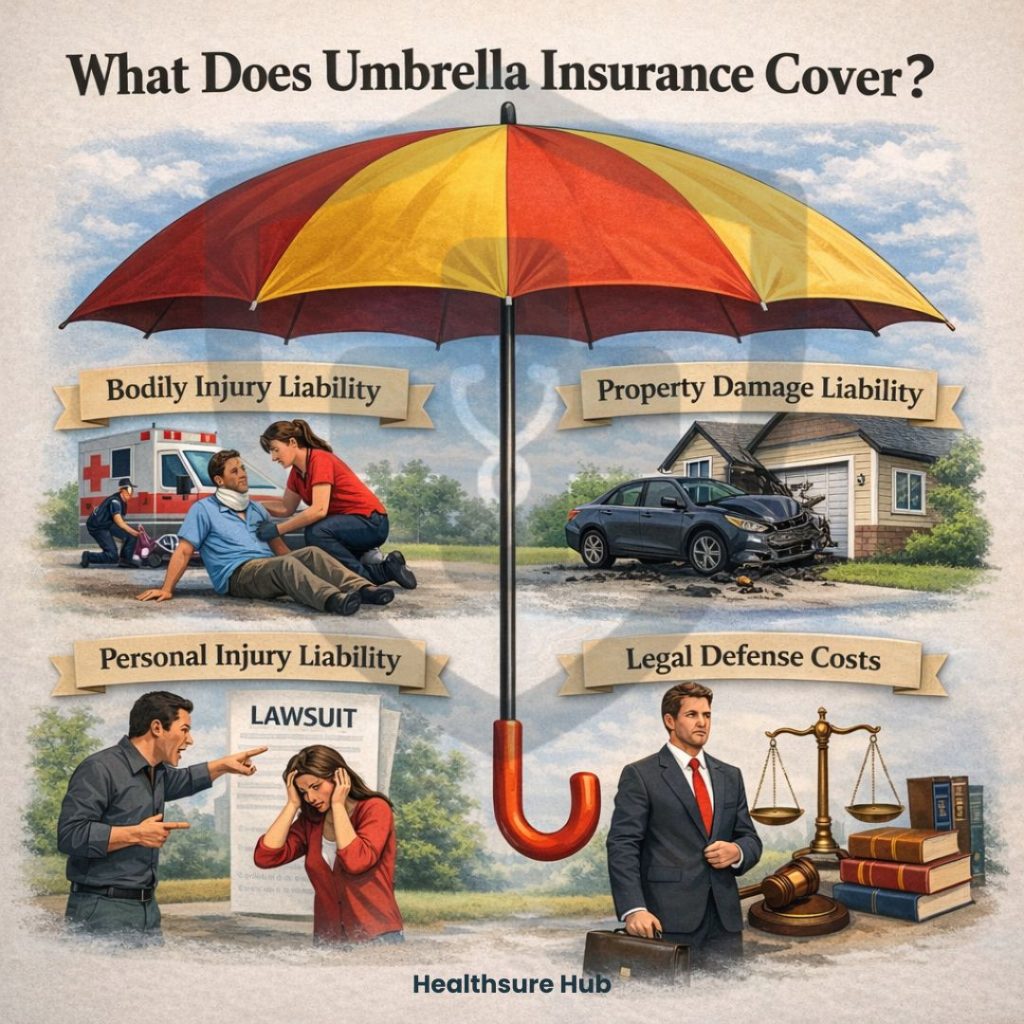

What Does Umbrella Insurance Cover?

With between 96% and 97% of all homeowners insurance claims involving damage to the home or personal property, umbrella insurance covers a wide range of liabilities, providing financial protection in situations where your primary insurance falls short. Knowing what does umbrella insurance cover is essential to fully understand its benefits. It generally covers:

Primary Liability Coverages

Bodily Injury Liability

Bodily injury coverage protects you if someone is injured and holds you responsible. This includes medical bills, rehabilitation costs, and loss of income due to an accident for which you are liable. Umbrella insurance ensures that even if the costs exceed your auto or homeowners policy limits, the remaining expenses are covered.

Property Damage Liability

If you accidentally damage someone else’s property, umbrella insurance covers the additional costs beyond your existing policy. This can include repairing a neighbor’s home after a fire, replacing a vehicle damaged in an accident, or covering other tangible property losses.

Personal Injury Liability

Personal injury coverage addresses claims such as libel or slander, defamation, and invasion of privacy. Many standard policies exclude these risks, but umbrella insurance ensures you are protected against lawsuits arising from false statements or personal reputation claims.

Legal Defense Costs

Even if you are not found liable, legal defense costs can be significant. Umbrella policies cover attorney fees, court costs, and other related expenses, ensuring that defending yourself does not drain your personal finances.

Additional Covered Situations

Besides the primary liability coverages umbrella insurance steps in in case of:

- Lawsuits – umbrella insurance steps in to cover lawsuits that surpass the limits of your underlying policies, protecting your assets and mitigating financial risk.

- Landlord Liability – if you own rental properties, umbrella insurance can extend coverage beyond standard landlord policies. This includes liability for injuries occurring on your rental property or claims arising from tenant incidents.

- Worldwide Liability Incidents – some umbrella policies provide global coverage, meaning liability claims arising from incidents occurring outside your home country may be covered.

- False Arrest or Detention Claims – umbrella insurance can also provide protection in unusual liability situations, such as false arrest, detention, or imprisonment claims, which are rarely included in standard insurance policies.

| Claim Type | Covered | Payment Type | Conditions |

| Bodily Injury | Yes | Medical bills, lost income, rehab costs | After underlying policy limits are met |

| Property Damage | Yes | Repairs or replacement | Only if damage exceeds primary policy coverage |

| Personal Injury | Yes | Legal fees, settlements | Includes slander, libel, invasion of privacy |

| Landlord Liability | Yes | Injury claims from tenants/guests | Optional coverage in some policies |

| Worldwide Liability | Yes | Legal and settlement costs | Some policies limit to specific countries |

| False Arrest/Detention | Yes | Legal costs | Only applies to non-criminal acts |

What Umbrella Insurance Does Not Cover

While umbrella insurance covers many high-cost liability scenarios, it does not cover everything. Knowing the exclusions helps avoid false assumptions and ensures you maintain adequate protection.

Personal Losses

Umbrella insurance does not cover injuries you sustain yourself or damage to your own property. For example, medical costs from your accident or repair costs for your home would still rely on your health or homeowners insurance.

Legal Exclusions

Criminal acts, intentional harm, and contractual disputes are generally excluded. If you intentionally damage property or violate a contract, the umbrella policy will not pay for related claims or legal fees.

Professional / Business Exclusions

Business liability, professional services, and malpractice claims are not typically covered under personal umbrella policies. Separate business insurance or a commercial umbrella policy would be required for these risks.

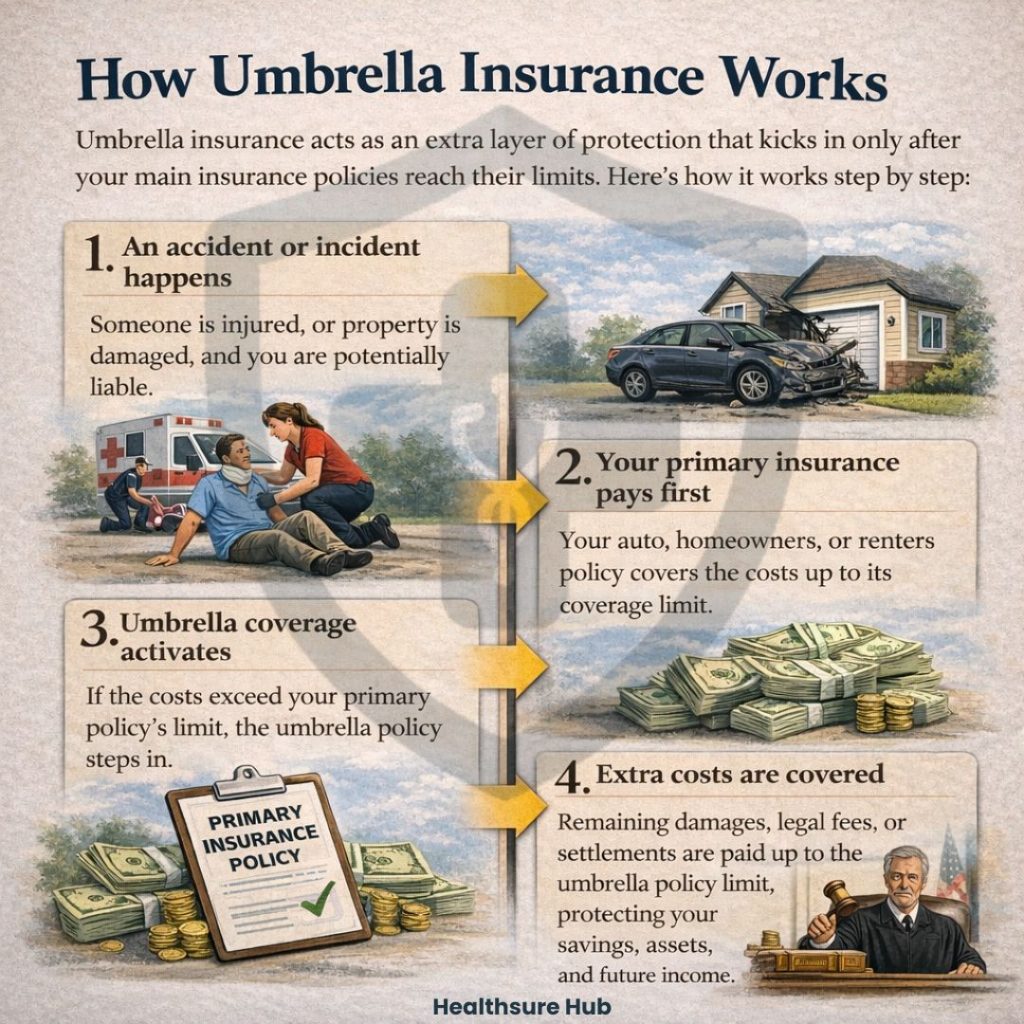

How Umbrella Insurance Works

Looking into what does umbrella insurance cover and how it works, you’ll find that it provides extra liability protection beyond your standard policies, helping safeguard your assets in the event of major claims or lawsuits. Umbrella insurance acts as an extra layer of protection that kicks in only after your main insurance policies reach their limits. Here’s how it works step by step:

- An accident or incident happens. Someone is injured, or property is damaged, and you are potentially liable.

- Your primary insurance pays first. Your auto, homeowners, or renters policy covers the costs up to its coverage limit.

- Umbrella coverage activates. If the costs exceed your primary policy’s limit, the umbrella policy steps in.

- Extra costs are covered. Remaining damages, legal fees, or settlements are paid up to the umbrella policy limit, protecting your savings, assets, and future income.

This layered system ensures you’re not left paying huge bills out-of-pocket, even in serious accidents or lawsuits, giving you peace of mind and financial security.

How Much Umbrella Insurance Coverage Do You Need?

Determining how much coverage you need involves evaluating your total assets and potential liability exposure. A simple calculation is:

Recommended Umbrella Coverage = Total Assets + Liability Exposure Risk

Consider the following:

- Savings and investments – Protect retirement accounts and liquid assets.

- Property value – Include your primary home, vacation homes, and rental properties.

- Vehicles – Auto and recreational vehicles contribute to liability risk.

- Future earnings potential – High income could be garnished in a lawsuit.

Most individuals start with $1 million in coverage, but high-net-worth households may require $5 million or more depending on exposure. Understanding what does umbrella insurance cover in relation to your assets helps determine the right limit.

How Much Does Umbrella Insurance Cost?

Average Premium Ranges

A $1 million umbrella policy typically costs between $250 and $500 per year. Higher-limit policies, like $5 million coverage, often remain affordable, ranging between $600 and $1,000 annually.

Cost Influencing Factors

Premiums are influenced by multiple factors:

- Claims history – prior liability claims can raise premiums.

- Driving record – accidents or violations increase risk.

- Property ownership – pools, trampolines, and rental properties increase liability.

- Liability exposure – active lifestyle or public-facing roles can affect cost.

- Credit profile – some insurers factor creditworthiness into pricing.

Despite these variables, umbrella insurance remains one of the most cost-effective ways to protect substantial assets. Understanding what does umbrella insurance cover in relation to your assets helps determine the right limit.

Common Mistakes to Avoid

To maximize the protection of umbrella insurance, avoid these pitfalls:

- Insufficient coverage limits – underestimating your potential liability can leave you exposed.

- Failing to raise base policy limits – umbrella insurance only activates after underlying policies are exhausted.

- Misunderstanding exclusions – knowing what is and isn’t covered prevents costly surprises.

- Assuming all liability situations are covered – intentional acts, business losses, and contractual disputes are excluded.

Proper understanding ensures that your umbrella policy delivers true financial security.

Conclusion

Umbrella insurance provides an essential safety net, covering liability beyond standard auto, homeowners, or renters policies. It protects against bodily injury, property damage, personal injury claims, legal defense costs, landlord liability, worldwide incidents, and false arrest claims. By supplementing existing coverage, it safeguards your assets, income, and financial stability. Understanding what does umbrella insurance cover is key for anyone seeking long-term protection against high-cost lawsuits and unexpected liabilities.