Every time you get behind the wheel, you accept a level of financial risk that most drivers rarely think about. A single accident can lead to thousands of dollars in vehicle repairs, medical bills, property damage, or legal claims. Without the right protection, one unexpected moment on the road can quickly turn into a major financial setback.

This is exactly what auto insurance is designed to prevent. While many people view insurance as just another monthly bill, the reality is far more important. Understanding what is the purpose of auto insurance helps drivers see how it protects their finances, manages liability after accidents, and provides critical support when something goes wrong.

Why Auto Insurance Exists

To fully understand what is the purpose of auto insurance, it helps to examine the risks associated with driving. Operating a vehicle always involves uncertainty. Even experienced drivers can encounter hazards such as distracted motorists, unpredictable weather conditions, road obstacles, or mechanical failures. These factors make accidents a possibility on any roadway.

The financial consequences of vehicle accidents can be substantial. According to the National Highway Traffic Safety Administration (NHTSA), as per the latest statistics, motor vehicle crashes in the United States alone result in $871 billion in economic loss and societal impact. Even minor collisions can cost thousands of dollars in repair expenses, while serious accidents involving injuries can escalate into tens or hundreds of thousands of dollars in liability claims.

Auto insurance systems developed to address these risks. By requiring or encouraging drivers to carry coverage, societies create a financial safety structure that ensures accident costs do not fall entirely on individuals who may not be able to afford them. This approach promotes accountability while helping maintain stability in transportation systems.

What is the Purpose of Auto Insurance?

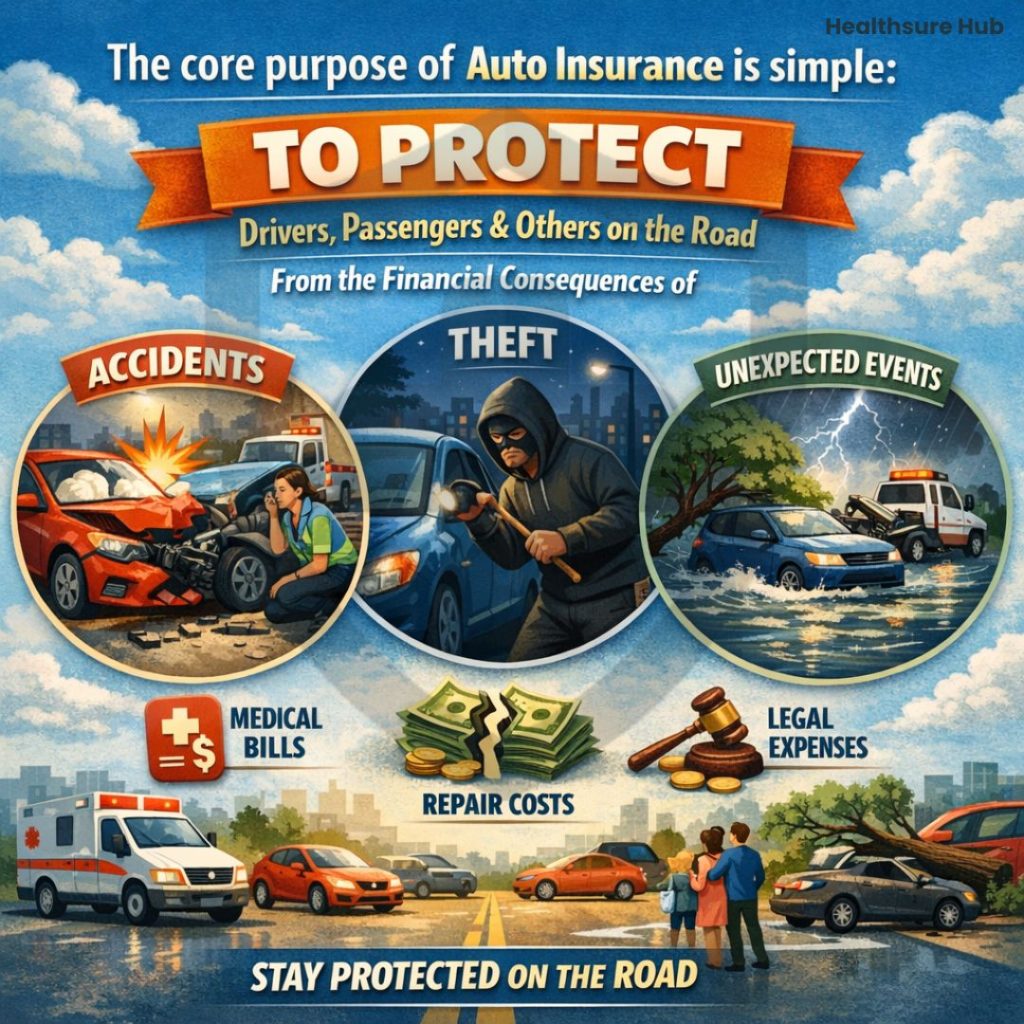

The core purpose of auto insurance is simple: to protect drivers, passengers, and others on the road from the financial consequences of accidents, theft, or unexpected events. This protection comes in three essential forms: financial protection, liability protection, and vehicle protection. Together, they form the foundation of modern car insurance policies.

Financial Protection

Financial protection is the most immediate benefit. Auto insurance protects drivers from sudden financial losses that can occur after an accident, vehicle theft, or severe weather damage. Without coverage, drivers would need to pay these expenses entirely out of pocket, which could create serious financial hardship.

Liability Protection

When a driver causes an accident, liability coverage helps pay for the injuries or property damage suffered by other people. This ensures that victims receive compensation for medical treatment, vehicle repairs, and other related costs. Liability protection also helps prevent lengthy legal disputes by providing a structured method for resolving claims.

Vehicle Protection

Vehicle protection adds another layer of security. Optional coverage options such as collision and comprehensive insurance help pay for repairs or replacement if the policyholder’s vehicle is damaged by accidents, theft, vandalism, falling objects, fire, or natural disasters. This protection helps drivers recover more quickly after unexpected events.

Together, these forms of coverage demonstrate clearly what is the purpose of auto insurance: to protect people financially while maintaining responsibility on the road.

How Auto Insurance Protects Drivers Financially

One of the most practical ways to understand what is the purpose of auto insurance is to examine the real financial impact of car accidents. Vehicle collisions are not only the leading cause of thousands of injuries but they often generate multiple types of expenses that can quickly accumulate.

Repairing damaged vehicles represents one of the most immediate costs. Modern cars include advanced technology, sensors, and safety systems that can make repairs surprisingly expensive. Even moderate damage to a bumper, headlights, or body panels can result in repair bills reaching several thousand dollars.

Medical expenses can increase the financial impact significantly. Injuries from car accidents may require emergency medical care, hospital treatment, rehabilitation, and long-term therapy. These healthcare costs can quickly exceed what most individuals could comfortably afford without insurance coverage.

Legal liability claims also play a role. When a driver is responsible for an accident that injures another person or damages property, the resulting legal claims can involve compensation for medical bills, lost wages, vehicle repairs, and pain and suffering. Without auto insurance, drivers may be personally responsible for paying these costs.

One of the best ways to understand this financial impact is by looking at real-world auto insurance claims statistics, which show how frequently accidents occur and how quickly costs can escalate across different types of claims.

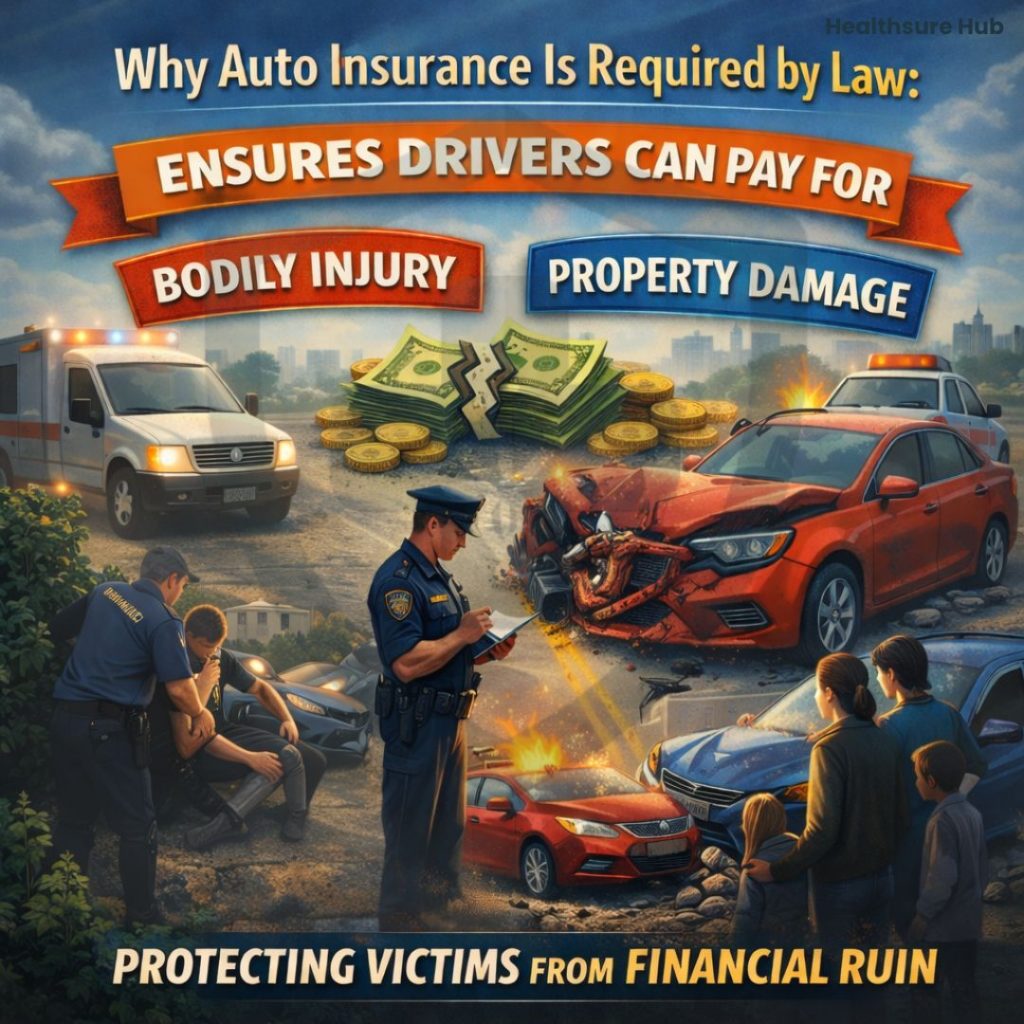

Why Auto Insurance Is Required by Law

Many governments require drivers to carry minimum levels of auto insurance before operating a vehicle on public roads.

While auto insurance doesn’t cover mechanical breakdown, the primary goal of these laws is to protect accident victims. If someone is injured or their vehicle is damaged by another driver, mandatory insurance ensures that compensation is available to cover medical expenses and property repairs. Without these requirements, accident victims might struggle to recover losses if the responsible driver lacked the financial resources to pay.

Mandatory insurance also encourages financial responsibility among drivers. By requiring coverage, governments ensure that motorists acknowledge the potential risks associated with driving and prepare for them responsibly.

In addition, insurance requirements help reduce legal conflicts after accidents. Instead of relying solely on court cases or personal negotiations, insurance policies provide a structured claims process that helps resolve disputes efficiently.

How Risk Transfer Works in Auto Insurance

When drivers purchase auto insurance, they pay premiums to an insurance company. These premiums contribute to a large pool of funds collected from thousands or even millions of policyholders. Because not every driver experiences an accident at the same time, insurers can use this pooled money to pay claims for those who do experience losses.

This system allows risk to be shared among many drivers rather than falling entirely on one individual. If a policyholder experiences a serious accident, the financial burden is supported by the broader insurance pool rather than by the driver alone.

What Auto Insurance Typically Covers

Although policies vary depending on location and provider, most auto insurance plans include several core types of coverage that support the broader purpose of protection. Optional coverages like rental reimbursement or loss of use protection can also help cover expenses when your vehicle is damaged and you need alternate transportation, adding another layer to how auto insurance supports drivers after a loss.

Liability Coverage

Liability coverage forms the foundation of most policies. It pays for injuries and property damage caused to other people if the insured driver is responsible for an accident. This coverage often includes bodily injury liability and property damage liability.

Collision Coverage

Collision coverage focuses on repairing or replacing the policyholder’s vehicle after a crash with another vehicle or object. It applies regardless of who is at fault in the accident, which helps drivers restore their vehicles more quickly.

Comprehensive Coverage

Comprehensive coverage addresses non-collision events such as theft, vandalism, fire, hailstorms, falling objects, or animal collisions. This type of coverage helps protect vehicles from a wide range of unexpected risks.

Medical payments coverage or personal injury protection may also be included in some policies. These options help pay for medical expenses resulting from accidents, covering drivers and passengers regardless of fault.

What Happens If You Drive Without Auto Insurance

If an uninsured driver causes an accident, they may be personally responsible for all damages, including vehicle repairs, medical expenses, and liability claims. These costs can quickly escalate beyond what many individuals can afford.

Legal penalties can also apply. Many jurisdictions impose fines, license suspension, or vehicle impoundment for drivers who fail to maintain required insurance coverage. In Washington for instance you could pay up to $550 or more in fines for a first offense. Repeated violations may lead to more severe consequences, including higher future insurance premiums.

Beyond the legal implications, uninsured driving increases uncertainty for everyone on the road. Without insurance coverage, accident victims may struggle to recover losses if the responsible driver cannot pay.

Conclusion

Understanding what is the purpose of auto insurance helps drivers recognize that coverage is more than a legal requirement. It provides financial protection after accidents, covers liability for injuries or property damage, and supports the repair or replacement of damaged vehicles.

In essence, what is the purpose of auto insurance is to create a financial safety net that protects drivers, passengers, and others on the road while ensuring accident victims can recover their losses. By understanding this role, drivers can make more informed decisions about coverage and approach driving with greater confidence and responsibility.